Management accounting is one of those disciplines that gets misrepresented almost everywhere it is taught. Most students hear "accounting" and picture spreadsheets full of historical transactions. What is management accounting, really? It is an internal process of collecting, analyzing, and presenting financial and operational data to help managers plan, control operations, and make strategic decisions. This guide breaks down its definition, core functions, key techniques, and real applications so you walk away with a working understanding of how it actually shapes business outcomes.

Table of Contents

- Key takeaways

- What management accounting actually means

- Core functions and techniques you need to know

- The role of a management accountant

- How management accounting works in practice

- My take on what students get wrong about this field

- How Amcfo applies these principles for your business

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Internal focus, future-oriented | Management accounting serves internal managers and prioritizes forward-looking data over historical records. |

| No external compliance required | Unlike financial accounting, it is not bound by GAAP or IFRS, which gives teams flexibility to tailor reports. |

| Covers more than cost tracking | Functions include budgeting, variance analysis, scenario planning, and performance evaluation. |

| Timeliness beats perfection | A timely estimate delivered this week is more useful to a manager than a precise figure delivered next month. |

| Strategic partner role | Management accountants work alongside leadership teams to turn financial data into decisions that drive growth. |

What management accounting actually means

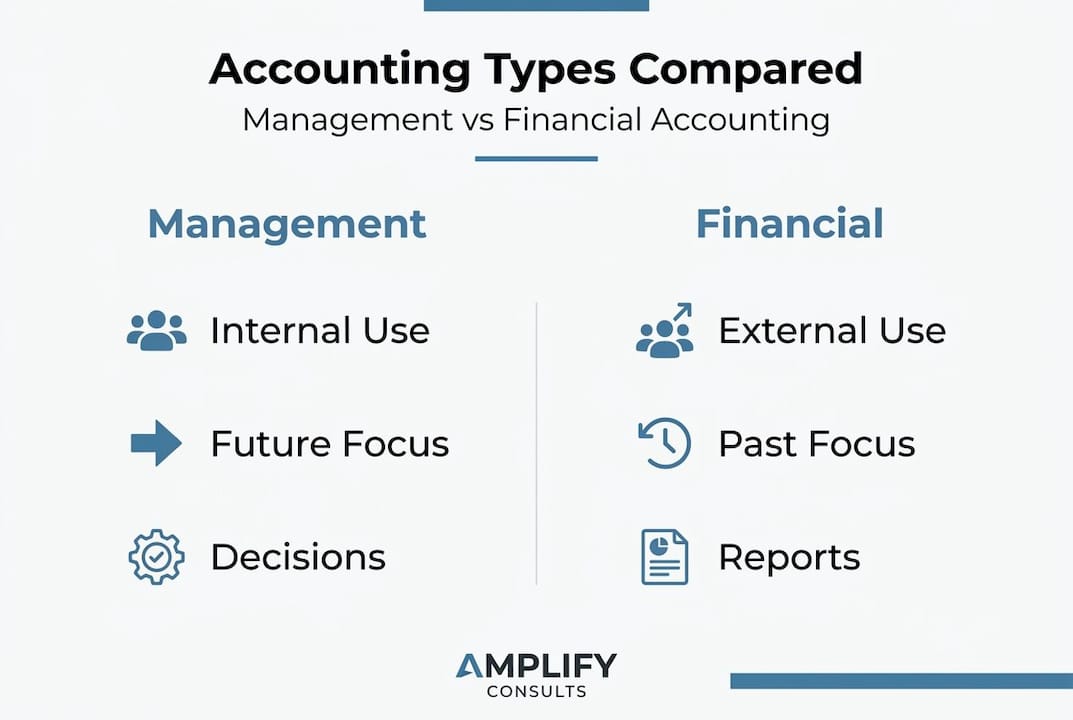

The definition of management accounting centers on one idea: financial information exists to improve decisions, not just to satisfy regulators. Where financial accounting produces reports for shareholders, lenders, and the IRS, management accounting produces reports for the people running the business. The audience is entirely internal.

That single difference changes everything. Financial accounting follows strict rules. Management accounting does not. Reports can be generated in any format, at any frequency, emphasizing whatever information the management team actually needs. A retail chain might generate a weekly store-by-store margin report. A manufacturing company might pull a daily variance report on raw material costs. Neither format exists in a textbook. Both are management accounting.

The scope covers four broad areas:

- Cost control: Tracking where money is being spent and whether that spending is justified

- Budgeting: Building financial plans that connect resource allocation to business goals

- Forecasting: Projecting future revenues, expenses, and cash positions based on current data

- Performance evaluation: Measuring results against targets and identifying what is working or not

Here is how management accounting compares to financial accounting at a glance:

| Feature | Management accounting | Financial accounting |

|---|---|---|

| Primary audience | Internal managers | External stakeholders |

| Reporting frequency | Weekly, monthly, or on demand | Quarterly or annually |

| Regulatory requirement | None | GAAP or IFRS compliance required |

| Data orientation | Future-focused | Historically based |

| Format flexibility | Fully customizable | Standardized formats |

| Accuracy vs. timeliness | Timeliness is prioritized | Accuracy is required |

One thing worth understanding early: management accounting does not replace financial accounting. It works alongside it, pulling from the same raw data but reshaping it to answer operational questions instead of compliance ones.

Core functions and techniques you need to know

The primary functions of management accounting include cost analysis, budgeting, variance analysis, and strategic planning. Each one feeds the others. Here is how they work in practice:

-

Cost analysis identifies which products, services, customers, or departments are profitable and which are draining resources. Activity-based costing (ABC) is one of the most widely used techniques here. Instead of spreading overhead costs evenly, ABC assigns costs based on actual activities, giving you a much sharper picture of where money really goes.

-

Budgeting translates business goals into financial targets. A well-built budget is not just a constraint. It is a communication tool. When every department head understands their budget in relation to company strategy, decision-making gets faster and more consistent.

-

Variance analysis compares actual results to budgeted figures and investigates the gap. If your cost of goods sold came in 12% above budget, variance analysis tells you whether that was a volume issue, a price issue, or both. That distinction changes what action you take.

-

Capital budgeting evaluates major investments like equipment purchases, facility expansions, or technology upgrades. Techniques like net present value (NPV) and internal rate of return (IRR) help management decide whether a long-term investment makes financial sense before committing.

-

Cost-Volume-Profit (CVP) analysis examines how changes in volume and cost affect profit. It answers questions like: "What is our break-even point?" and "How much do sales need to grow before this new product line becomes profitable?"

Management accounting reports are often generated weekly or monthly rather than annually, which gives managers the feedback they need to act on problems before they compound. That frequency is one of management accounting's biggest advantages over traditional financial reporting.

Pro Tip: When learning variance analysis, always separate price variances from volume variances. A favorable cost variance caused by buying less material is very different from one caused by negotiating a lower price. Conflating them leads to wrong conclusions.

The role of a management accountant

There is a persistent misconception that management accountants sit in back offices generating reports nobody reads. The actual role looks nothing like that. Modern management accountants function as business partners and internal consultants. They sit in strategy meetings, challenge assumptions, and translate financial data into language that operations managers, sales directors, and product teams can actually use.

Effective management accountants translate complex financial data into non-financial insights that department heads can act on. That means a production manager does not need to understand contribution margin accounting. They need to understand that running a third shift adds $40,000 in overhead and only generates $28,000 in additional revenue. The management accountant is the person who figures that out and communicates it clearly.

The role also requires a specific kind of balance. Management accountants often serve as a counterweight to ambitious leadership. A visionary CEO might see a market expansion opportunity. The management accountant asks: do we have the cash reserves for this? Can our operations support the demand? They provide financial reality checks that keep growth sustainable rather than reckless.

Key skills that separate strong management accountants from average ones include:

- Translating financial models into plain business language

- Understanding operations well enough to spot when numbers do not match reality

- Building trust with non-finance colleagues so that their analysis actually gets used

- Knowing when to push back on leadership and when to adapt the analysis

"Management accounting is the internal compass of a business, blending technical accounting skills with commercial insight." — Robert Half

That quote captures the professional identity well. You are not just an accountant. You are a commercial advisor who happens to work with numbers.

How management accounting works in practice

Knowing the theory is useful. Seeing how it plays out in real business situations is what makes it stick. Here are four common scenarios where management accounting directly shapes decisions.

Budgeting and resource allocation

A company is planning for the upcoming fiscal year. The management accountant builds a financial forecasting process that ties departmental budgets to projected revenue, factoring in seasonality, headcount changes, and capital needs. Without this structure, departments request what they want. With it, every dollar requested has to connect back to a business outcome.

Performance evaluation

Mid-year, actual revenue is 15% below forecast. Variance analysis pinpoints which product lines are underperforming, whether the gap is price-driven or volume-driven, and which markets are holding steady. That level of detail tells leadership exactly where to intervene rather than cutting costs across the board indiscriminately.

Scenario planning

A business is considering launching a new service line. The management accountant runs three scenarios: optimistic, base case, and conservative. Each scenario maps out the cash requirements, break-even timeline, and margin impact. Leadership can then make a go or no-go decision with a clear view of the financial range they are accepting.

Cost reduction

A company suspects its customer service operation is expensive relative to output. Efficiency and cost analysis compares cost per ticket resolved, identifies the most expensive service categories, and surfaces whether automation or staffing changes would produce better economics. The output is a specific, defensible recommendation rather than a vague call to "cut costs."

Pro Tip: The most powerful management accounting reports are the ones that include a recommended action, not just data. When you present a variance analysis, always pair it with at least one hypothesis about the cause and one suggested response. That is what turns reporting into advising.

Here is a quick reference for which techniques apply to which business decisions:

| Business question | Relevant technique |

|---|---|

| Are we making money on this product? | Margin analysis, activity-based costing |

| Should we invest in new equipment? | Capital budgeting, NPV analysis |

| Why did costs exceed budget? | Variance analysis |

| What sales volume do we need to break even? | CVP analysis |

| How should we allocate next year's budget? | Zero-based or incremental budgeting |

Management accounting data reports regularly cover cash on hand, capital budgeting analyses, inventory accuracy, loan covenant compliance, and project profitability. The format is always built around what the specific manager needs to decide, not what looks good in a standard template.

My take on what students get wrong about this field

I have worked with business students and early-career professionals long enough to spot the pattern. Most come in thinking management accounting is just "internal financial reporting." It takes time before they realize it is actually a consultative function. That shift in understanding changes how you approach the work entirely.

What I have seen hold people back most is the comfort with data and the discomfort with communication. A student can build a spotless variance model but struggle to walk a department head through it in two minutes. In practice, the communication is the job. The model is just the preparation.

I also think the flexibility of management accounting is underestimated early on. Management accounting prioritizes timeliness over perfect accuracy, and that is a deliberate feature, not a flaw. Students trained on GAAP-compliant financial accounting sometimes feel uncomfortable with estimates and approximations. Getting over that discomfort is what separates good management accountants from great ones.

One more thing worth saying out loud: sustainability is becoming a strategic input in management accounting, not just a reporting footnote. The professionals who will be most valuable in the next decade are the ones who can build a business case around ESG investments and tie them to financial outcomes. That is a management accounting problem. Start thinking about it now.

— Angelica

How Amcfo applies these principles for your business

If you are past the theory and looking for the practice, Amcfo applies management accounting principles directly in the work we do with clients every day.

Our fractional CFO services bring strategic financial leadership to businesses that need it without the overhead of a full-time hire. That includes budgeting, forecasting, variance analysis, scenario planning, and cost control. Our accounting and bookkeeping services keep your financial data clean and timely so that management reporting is actually reliable. And our business consulting team works alongside leadership to turn financial analysis into decisions that move the business forward. If you want to put management accounting to work in your organization, we are ready to help.

FAQ

What is the definition of management accounting?

Management accounting is the process of collecting, analyzing, and presenting financial and operational data to help internal managers plan, control costs, and make strategic decisions. It is not bound by external accounting standards and can be tailored to whatever information a business needs.

How does management accounting differ from financial accounting?

Financial accounting produces standardized reports for external stakeholders and follows GAAP or IFRS. Management accounting produces flexible, internally focused reports for business leaders, prioritizing timeliness and relevance over regulatory compliance.

What are the main management accounting techniques?

Common techniques include activity-based costing, Cost-Volume-Profit analysis, variance analysis, margin analysis, and capital budgeting. Each one addresses a specific type of business decision, from pricing to investment evaluation.

Why is management accounting important for businesses?

Management accounting gives leadership the specific financial insights they need to allocate resources, control costs, evaluate performance, and plan strategically. Without it, decisions get made on intuition rather than data.

What does a management accountant actually do?

A management accountant analyzes financial data, builds budgets and forecasts, investigates performance variances, and translates complex financial information into clear recommendations for non-finance managers and leadership teams.