Most small business owners feel confident about their financial future, yet 94% of SME owners feel prepared 12 to 18 months ahead while only 24% actually have more than six months of emergency savings. That gap between perceived confidence and real preparedness is where businesses get hurt. Financial risk management is the structured discipline of identifying, analyzing, and responding to threats before they damage your cash flow, operations, or growth potential. This guide walks you through proven frameworks, practical strategies, and the specific benchmarks that turn financial anxiety into informed decision-making.

Table of Contents

- Understanding financial risk: What it means for your business

- Core frameworks: ISO 31000 and COSO ERM explained

- Essential risk management strategies for SMEs

- Risk treatment options: Making the right call

- Benchmarking and monitoring your financial risks

- Why most business owners underestimate risk — and how to shift your mindset

- Take the next step: Professional support for your financial peace of mind

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Risk identification is crucial | The first step to managing financial risk is understanding your unique exposure. |

| Use frameworks for guidance | Proven models like ISO 31000 and COSO ERM provide reliable structures for risk management. |

| Maintain a cash buffer | A 3–6 month cash reserve protects your business from sudden financial shocks. |

| Benchmark and monitor | Tracking ratios like DSO and CCC helps ensure your business stays financially healthy. |

| Expert support adds value | Professional guidance can uncover hidden risks and boost your business’s resilience. |

Understanding financial risk: What it means for your business

With risk preparedness often overestimated, it's critical to understand what financial risk is and why it matters to your business. Financial risk management is not just about preventing disasters. It is the ongoing process of understanding every financial threat your business faces and deciding, deliberately, how to handle each one. Think of it as business financial management at its most strategic level.

The most common financial risks for SMEs include:

- Cash flow shortfalls: Revenue arrives late, but bills do not wait.

- Credit risk: Customers fail to pay, straining your working capital.

- Fraud exposure: More than half of small business owners have already faced fraud attempts.

- Market changes: Interest rate shifts, supply chain disruptions, or economic downturns erode margins.

- Compliance failures: Tax penalties, payroll errors, or licensing lapses create surprise costs.

"A structured risk approach removes guesswork. When you have a process, a cash crisis becomes a managed event rather than an emergency."

Why does a systematic approach matter so much? Without structure, most owners react rather than prepare. They fix the leak after the ceiling collapses. Structured risk management strategies overview force you to identify vulnerabilities on a schedule, assign responsibility, and track whether your controls are actually working.

Two globally recognized methodologies define this structure. The ISO 31000 standard follows a disciplined cycle of communication, context setting, risk identification, analysis, evaluation, treatment, monitoring, and reporting. The COSO ERM framework takes a broader view, integrating risk directly into strategy through five components: governance and culture, strategy and objective setting, performance, review and revision, and information and communication. Both approaches reduce panic and increase precision.

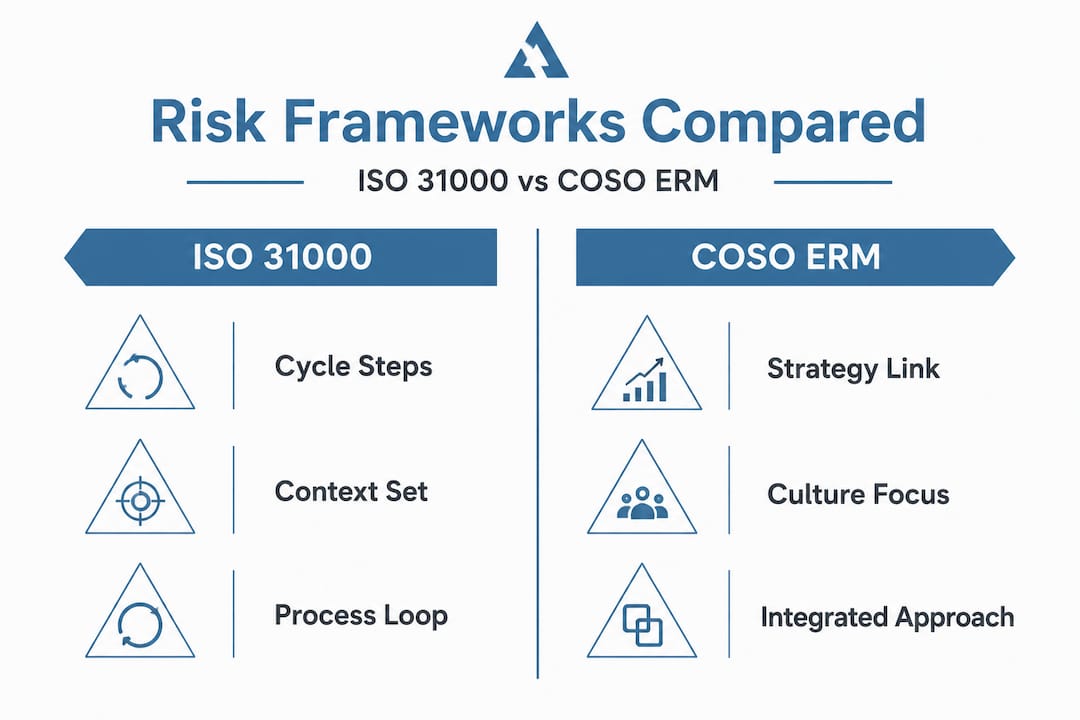

Core frameworks: ISO 31000 and COSO ERM explained

Now that you know why financial risk management matters, let's look at the leading frameworks that bring structure to the process. These two models are not just for large corporations. Their principles scale down cleanly for any SME willing to apply them.

ISO 31000 in plain English

ISO 31000 gives you a repeatable process loop. You start by setting context (who you are, what you're protecting, what environment you operate in), then identify risks, analyze their probability and impact, evaluate which ones need action, treat the priority risks, and monitor results over time. Every step is documented. This documentation is what turns risk management into organizational memory instead of individual instinct.

COSO ERM in plain English

COSO ERM connects risk directly to your strategy. It asks: what are we trying to achieve, what could stop us, and how do we weave risk awareness into our daily decisions? Where ISO 31000 excels at process, COSO ERM excels at culture and leadership alignment.

| Feature | ISO 31000 | COSO ERM |

|---|---|---|

| Primary focus | Risk process cycle | Strategy and culture integration |

| Best for SMEs when | You need a step-by-step workflow | You want leadership alignment on risk |

| Documentation emphasis | High | Moderate |

| Integration with business goals | Moderate | Very high |

| Complexity for small teams | Low to medium | Medium |

Which should you use? Many SMEs benefit from starting with ISO 31000 to build the habit of structured structured risk management review, then layering in COSO ERM principles as the business grows and strategic planning becomes more formal.

Pro Tip: You do not need to formally certify under either framework to benefit from them. Even borrowing the core concepts, like running a quarterly risk identification session and tracking a short list of key threats, delivers measurable improvement in financial resilience.

Understanding ERM frameworks at even a surface level gives you a shared vocabulary with lenders, investors, and advisors. That vocabulary signals maturity and builds confidence in your business.

Essential risk management strategies for SMEs

Frameworks are only valuable if put into action. Here's how SMEs can apply key risk management strategies right now.

1. Build a rolling cash flow forecast

A 13 to 90 day rolling cash flow forecast is one of the most powerful tools available to any SME. It shows you, week by week, when money comes in and when it goes out. You can spot a dangerous gap three weeks in advance instead of discovering it on the day payroll is due. Review your cash flow management tips to get the mechanics right.

2. Maintain a 3 to 6 month cash buffer

Effective risk management for SMEs consistently identifies a 3 to 6 month operating expense reserve as a baseline for resilience. This buffer absorbs revenue delays, unexpected expenses, or short-term client loss without forcing you into emergency borrowing. The pitfall many owners hit: they build the buffer, then quietly draw it down during a slow quarter without replacing it. Treat it as untouchable except for genuine emergencies.

3. Use revolving credit and invoice finance strategically

A revolving credit facility gives you on-demand access to capital without committing to a fixed loan. Invoice finance (sometimes called accounts receivable financing) can advance up to 85% of an outstanding invoice's value before the customer pays. These tools bridge the gap between delivering work and receiving payment, a cycle that kills cash flow for service businesses in particular.

4. Apply credit controls rigorously

Set clear payment terms. Send invoices immediately. Follow up on overdue accounts on a schedule, not when you feel like it. Businesses that systematize credit controls dramatically reduce their Days Sales Outstanding (DSO), which is the average number of days it takes to collect payment after a sale.

5. Build your financial forecasting process into a regular rhythm

Forecasting should not be an annual event. Monthly or quarterly forecasts, updated with real data, allow you to adjust before problems compound. Use practical financial modeling tools to scenario-test your projections.

Here are the key benchmarks to track, drawn from JP Morgan's working capital data:

| Metric | Healthy range | Top quartile target |

|---|---|---|

| Current ratio | 1.2 to 2.0 | 1.8+ |

| Days Sales Outstanding (DSO) | Under 42 days | 30 to 34 days |

| Cash Conversion Cycle (CCC) | Under 50 days | 30 days or less |

The power of one day. According to JP Morgan's benchmarking research, one day of CCC improvement generates approximately $1 million in freed-up cash for a business with $365 million in annual revenue. For an SME, the proportional gain is still significant. Faster collection and smarter payment timing translate directly into available cash.

Pro Tip: If you're not sure where to start with financial management for entrepreneurs, benchmark your current DSO against the 42-day median. If you're above that, tightening collections alone can meaningfully improve your cash position within a single quarter.

Risk treatment options: Making the right call

Now that practical tools are on the table, the next decision is choosing the right way to address each risk. Not every risk deserves the same response. According to ISO 31000 principles, there are four core treatment options:

- Avoid: Stop doing the activity that creates the risk. If a particular client segment consistently pays late and consumes disproportionate collection effort, you may choose to stop serving them.

- Mitigate or reduce: Take action to lower the probability or impact of the risk. Tightening internal financial controls, adding approval layers for large transactions, or diversifying your customer base all reduce exposure.

- Share or transfer: Move the financial consequence of a risk to another party. Insurance is the classic example. For low-probability but high-impact events (a fire, a major lawsuit, a data breach), transferring the financial risk through insurance is often the most cost-effective response.

- Accept: Acknowledge that a risk exists, decide it is within tolerable limits, and monitor it without taking additional action. This is appropriate for low-probability, low-impact risks where the cost of mitigation outweighs the potential loss.

The most useful decision tool for prioritizing which treatment to apply is a likelihood versus impact matrix. Plot each identified risk on a two-axis grid: how likely it is to occur versus how damaging it would be if it did. High-likelihood and high-impact risks demand immediate action. Low-likelihood and low-impact risks can be accepted and monitored.

Smart risk treatment often involves mixing strategies. You might mitigate fraud risk through internal controls while simultaneously transferring residual risk through crime insurance. You might accept minor accounts receivable delays for long-term clients while applying strict credit controls for newer customers. Get expert business consulting if you're unsure how to prioritize your specific risk portfolio.

The risk management workflow behind these decisions does not have to be complex. A simple, documented process reviewed quarterly is far more effective than a sophisticated system reviewed never.

Benchmarking and monitoring your financial risks

With risk treatment underway, it's vital to ensure your plan is actually working. Continuous monitoring and benchmarking make this possible. Risk management is not a set-and-forget exercise. Markets change, customers change, and your business changes. The controls that worked last year may not cover new exposures this year.

Here is why ongoing monitoring matters and what to track:

- Stay alert to new risks early: Regular reviews surface emerging threats before they become crises.

- Validate that controls are working: Monitoring tells you whether your credit controls are actually reducing DSO or just adding paperwork.

- Demonstrate accountability: Documented monitoring gives lenders and investors evidence that you manage your business proactively.

- Enable faster course correction: When you track metrics consistently, you spot negative trends early enough to act.

The benchmarks that matter most, according to JP Morgan's working capital research, are your current ratio (target 1.2 to 2.0), your DSO (top quartile is 30 to 34 days versus a median of 42), and your cash conversion cycle (leaders run 30 to 50 days shorter than average performers).

| Benchmark | What it measures | Action if off target |

|---|---|---|

| Current ratio below 1.2 | Liquidity risk | Review payables and build cash reserves |

| DSO above 42 days | Collection efficiency | Tighten invoicing and follow-up process |

| CCC trending up | Working capital strain | Accelerate receivables, renegotiate payables |

Top-performing businesses use automation to optimize workflows, enabling 20 to 30% DSO reductions compared to manual processes. Your process optimization tips and efficiency analysis both become easier when you have live metrics to work from rather than month-old reports.

Why most business owners underestimate risk — and how to shift your mindset

This all leads to an important realization. Success is not just about following steps. It is about how you see and approach risk over the long term.

Here is the uncomfortable truth: confidence can be a liability. The TD 2026 survey gap between "feeling prepared" (94%) and "actually having a safety net" (24%) is not caused by laziness. It is caused by something far more human: optimism bias. Business owners are, by nature, optimists. That optimism drives them to start companies and weather hard times. But it also causes them to underestimate how long a bad month, a fraud attempt, or a slow-paying client can disrupt cash flow.

In financial advisory work, two patterns appear repeatedly. The first is what we call the "busy trap." Owners know they should build better financial controls, but day-to-day operations consume every hour. Risk management becomes tomorrow's project indefinitely. The second pattern is "false precision." Business owners look at last year's results, see that things were fine, and assume this year will be similar. But past stability is not the same as future resilience.

What do businesses that recover quickly from financial shocks have in common? They treat risk review as a fixed calendar event, not a reactive response. They know their current ratio before their accountant tells them. They have already thought through what they would do if their top three clients paused payments simultaneously. That kind of proactive planning, supported by growth consulting insights, is not pessimism. It is the foundation of genuine confidence.

The mindset shift is simple but rarely made: stop measuring preparedness by how optimistic you feel, and start measuring it by what your actual numbers show.

Take the next step: Professional support for your financial peace of mind

Understanding risk frameworks and benchmarks is the first move. The second is having the right team to help you implement them consistently and correctly.

At AmCFO, we work with small and medium-sized businesses that want to close the gap between knowing what good risk management looks like and actually having it in place. Whether you need fractional CFO support to build a rolling forecast and risk review process, bookkeeping and accounting services to ensure your financial data is accurate enough to benchmark, or a detailed cost efficiency analysis to identify where money is leaking, we can build the right combination of support for your business. Reach out today and let's turn your financial data into a genuine risk management advantage.

Frequently asked questions

What is the first step in financial risk management for my business?

The first step is to identify and assess your core financial risks, using a structured framework such as ISO 31000 or COSO ERM to guide the process consistently.

How much of a cash buffer should small businesses keep?

Businesses are generally advised to keep a cash buffer covering 3 to 6 months of operating expenses to absorb unexpected disruptions without resorting to emergency borrowing.

Which risk management frameworks are best for SMEs?

ISO 31000 and COSO ERM are both recommended because the COSO ERM framework integrates risk with strategy, while ISO 31000 offers a clear process cycle that scales to any business size.

What financial benchmarks should I monitor?

Key benchmarks include your current ratio (target 1.2 to 2.0), Days Sales Outstanding of 30 to 34 days for top performers, and your cash conversion cycle compared to your industry peers.

How can I reduce my business's exposure to financial fraud?

Implement strong internal controls and regular audits, because 54% of SME owners have already faced fraud attempts and basic process controls are the most effective first line of defense.