Running a business without a financial forecast is like driving at night with no headlights. You might make it, but every unexpected curve costs you. Many small and midsize business owners discover too late that strong revenue does not guarantee positive cash flow, and that missed forecasting opportunities translate directly into missed payroll, stalled growth, or costly emergency borrowing. A structured forecasting process fixes that. This guide walks you through the tools, steps, and expert shortcuts you need to build forecasts that actually drive better decisions.

Table of Contents

- Why financial forecasting matters for your business

- What you need: Tools, data, and assumptions

- Step-by-step financial forecasting process for SMBs

- Applying forecasting: Cash flow, scenarios, and common pitfalls

- Monitoring, updating, and extracting value from your forecast

- Why forecasting fails — and how SMBs can make it work

- Expert help to implement your forecasting process

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Start simple, track often | Begin with accessible data and a straightforward process, then keep forecasts updated for best results. |

| Pair profit with cash flow | Always build cash flow forecasts alongside profit projections to avoid surprises and match your business’s real timing. |

| Use scenarios, not guesses | Test base, upside, and downside cases to prepare your business for different realities and make stronger decisions. |

| Regular reviews drive value | Monitoring and refining your forecasts are essential for catching problems early and taking timely action. |

| Expert guidance pays off | Leveraging professional insight can elevate your forecasting and help unlock your business’s full growth potential. |

Why financial forecasting matters for your business

Most business owners think of forecasting as something large corporations do. That assumption is expensive. For small and midsize businesses, a forecast is often the difference between catching a cash shortfall three months early and scrambling to cover payroll on a Friday afternoon.

Forecasting reduces dangerous surprises by forcing you to map out expected inflows and outflows before they happen. When you see a potential gap forming in month four, you have time to accelerate collections, delay a purchase, or line up a credit facility. Without a forecast, you only see the gap when it arrives.

There is also a strategic side. Businesses that forecast regularly are more agile. When a new opportunity appears, such as a bulk order or a new market, you can quickly model whether your cash position supports it. That kind of speed is a real competitive advantage.

One distinction matters enormously here: cash forecasting is not the same as profit forecasting. Your income statement might show a profitable quarter while your bank account is nearly empty. That happens because accrual accounting records revenue when it is earned, not when cash arrives. A customer invoice due in 60 days shows up as revenue today but does not fund your rent payment next week.

Pairing your income projections with a cash flow forecast is not optional. It is the only way to see both your profitability picture and your real-time liquidity at the same time.

Key benefits of a consistent forecasting process:

- Early warning on cash gaps before they become crises

- Clearer basis for hiring, capital, and vendor decisions

- Stronger conversations with lenders and investors

- Better alignment between sales targets and operational capacity

- Confidence when evaluating growth opportunities

As the GFOA forecasting process outlines, a practical SMB forecasting process starts by defining purpose and assumptions, then analyzing historical data, selecting methods, building a model, and repeatedly monitoring results. That cycle is the foundation of everything that follows. Combining this with SME cash flow best practices gives you a complete picture of financial health.

What you need: Tools, data, and assumptions

Before you build anything, you need the right ingredients. Fortunately, most of what you need already exists inside your business.

Key data sources:

- Last 12 to 24 months of income statements and balance sheets

- Accounts receivable aging report (who owes you and when)

- Accounts payable schedule (what you owe and when it is due)

- Sales pipeline or signed contracts for forward-looking revenue

- Vendor agreements with fixed or variable cost schedules

- Payroll records and any known upcoming headcount changes

Tools you will use:

| Tool type | Best for | Example options |

|---|---|---|

| Spreadsheet templates | Simple, flexible models | Excel, Google Sheets |

| Accounting software | Pulling actuals automatically | QuickBooks, Xero |

| FP&A platforms | Larger or faster-growing SMBs | Planning tools built on your accounting data |

| CFO advisory support | Complex scenarios and decisions | Fractional CFO services |

Choosing your assumptions is where most business owners get stuck. Start with three: your expected revenue growth rate based on historical trends, your average customer payment timing (30, 45, or 60 days), and your known fixed costs. Then layer in seasonality if your business has predictable slow or busy periods. Refer to our financial modeling guide for a deeper look at how to structure these inputs.

Pro Tip: Do not try to forecast everything perfectly on day one. A model with three solid assumptions updated monthly beats a complex model that never gets touched.

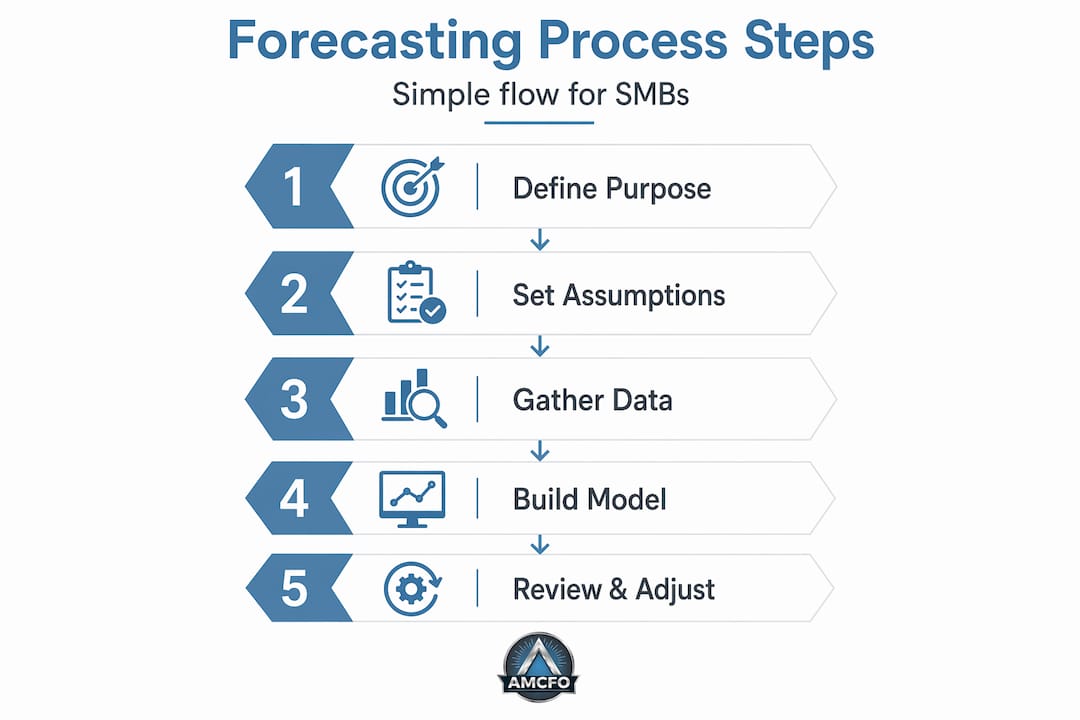

Step-by-step financial forecasting process for SMBs

With your data and tools ready, here is how to build your forecast from scratch.

- Define your purpose. Are you forecasting to manage cash, plan a hire, prepare for a loan, or guide annual planning? Your purpose shapes your time horizon and level of detail.

- Set your assumptions. Document your growth rate, payment terms, cost drivers, and any known one-time items. Write these down so you can test and revise them later.

- Pull and analyze historical data. Look for trends, seasonality, and anomalies in the past 12 to 24 months. This is your baseline.

- Choose your forecasting method. For cash flow, the direct method tracks actual cash transactions. The indirect method starts with net income and adjusts for non-cash items. For planning, driver-based forecasting links operational levers like units sold or headcount directly to financial outcomes, which makes your model more responsive to real business changes.

- Build your model. Start with a monthly income statement projection, then build a cash flow statement that reflects when cash actually moves.

- Run scenarios. Build at least three versions: base case, upside, and downside. This is not pessimism. It is preparation.

- Review and update on a schedule. Monthly for the first year, quarterly for years two and three.

Financial projections for SMBs are commonly structured as monthly for year one, quarterly for the next two years, and annual thereafter. This structure keeps detail where you need it most.

| Forecasting method | How it works | Best use case |

|---|---|---|

| Direct cash flow | Tracks actual cash in and out | Short-term liquidity management |

| Indirect cash flow | Adjusts net income for non-cash items | Longer-term planning tied to P&L |

| Driver-based | Links KPIs to financial outcomes | Growth modeling and hiring decisions |

| Scenario-based | Models multiple futures | Risk planning and investor conversations |

Pro Tip: Use cash flow forecast steps to structure your spreadsheet with an opening balance, then add inflows and subtract outflows for each period. This simple structure is the backbone of every strong cash forecast. When you are ready to connect your forecast to broader strategy, strategic growth consulting can help you translate numbers into action.

Applying forecasting: Cash flow, scenarios, and common pitfalls

Building the forecast is step one. Using it well is where the real value lives.

Direct vs. indirect cash flow forecasting:

The direct method is better for short-term cash management. You list every expected cash receipt and payment by week or month. The indirect method is better for longer planning horizons because it reconciles your profit forecast with cash movement. Most SMBs benefit from using both together.

Scenario planning in practice:

Build a cash flow forecast by structuring a spreadsheet with your opening balance, then modeling inflows and outflows for each period. Plan for best and worst cases, and update on a rolling basis every two to three months. A rolling 12-month view keeps your forecast always looking a full year ahead, no matter when you check it.

J.P. Morgan's guidance on cash forecasting reinforces this: use multiple scenarios with probabilistic thinking rather than forcing a single point estimate. This helps you prepare actions for bad-but-plausible outcomes before they arrive.

A single-point forecast is a false sense of certainty. Three scenarios give you a decision framework. That is the difference between reacting and leading.

Common mistakes to avoid:

- Over-optimism on revenue timing (assume slower collections than you hope for)

- Ignoring the lag between invoicing and cash receipt

- Treating the forecast as a one-time document instead of a living tool

- Skipping scenario planning because the base case looks fine

- Failing to connect your cash forecast to your financial management and planning process

Pro Tip: When building your downside scenario, ask yourself: "If our biggest customer paid 30 days late and our second-largest deal fell through, could we cover operations?" If the answer is no, that scenario needs a response plan attached to it.

Monitoring, updating, and extracting value from your forecast

A forecast you never update is just a document. A forecast you review monthly becomes a management tool.

- Set a recurring review date. Block time on your calendar, monthly at minimum. Treat it like a board meeting.

- Enter actuals and compare. Pull your real numbers from your accounting software and drop them next to your forecast. Where are you ahead? Where are you behind?

- Analyze the variance. A 10% miss on revenue is only useful information if you understand why it happened. Was it timing, a lost deal, or a pricing issue?

- Recalibrate your assumptions. If customers are consistently paying in 50 days instead of 30, update your model. Stale assumptions produce stale forecasts.

- Use the forecast in every key meeting. When you discuss hiring, marketing spend, or a new contract, open the forecast. Let the numbers inform the conversation.

The GFOA process framework emphasizes that monitoring and updating are not optional steps. They are what turns a forecast into a learning system. Pair this with driver-based modeling and you can see exactly which business levers are moving your financial outcomes.

Pro Tip: Schedule a 30-minute "forecast vs. actuals" review at the end of every month. Over time, this habit builds a feedback loop that makes your assumptions sharper and your decisions faster. If you want expert support structuring this process, fractional CFO services can help you build a review cadence that fits your business. Learn more about structuring that relationship in our guide to a CFO advisory engagement.

Why forecasting fails — and how SMBs can make it work

Here is something most forecasting guides will not tell you: the forecast itself rarely fails. The process around it does.

Most SMB forecasts fail because they were built once, filed away, and never touched again. The spreadsheet becomes a historical artifact instead of a live tool. Business owners then conclude that forecasting does not work for their size or industry. That conclusion is wrong.

The real problem is rigidity. A forecast built on a single set of assumptions, with no scenario thinking and no update schedule, cannot survive contact with reality. Markets shift. Customers pay late. A key vendor raises prices. A rigid forecast has no answer for any of that.

Scenario thinking changes the equation entirely. When you have a base case, an upside, and a downside already modeled, you are not surprised by variation. You are choosing which plan to execute. That mental shift from "what happened to my forecast" to "which scenario am I in now" is what separates businesses that use forecasting strategically from those that treat it as a compliance exercise.

The other lesson from working with SMBs is that the spreadsheet matters far less than the discipline. We have seen businesses run effective forecasts on a basic Google Sheet and others with expensive software that never looked at their numbers. The tool is not the differentiator. The habit is.

Avoid the financial modeling pitfalls that trap most small businesses: over-engineering the model before you have clean data, building for the best case only, and skipping the variance review that makes the whole process worthwhile.

Expert help to implement your forecasting process

Building a forecasting process from scratch takes time, and getting it right the first time matters.

At AmCFO, we work with small and midsize businesses every day to build forecasting systems that actually get used. Whether you need help setting up your first model, cleaning up your historical data, or running ongoing scenario analysis, our fractional CFO services give you senior-level financial expertise without the full-time cost. Our business consulting team can also connect your forecast to your broader growth strategy, so your numbers and your plans move together. If you are ready to stop guessing and start leading with data, explore our financial management and planning services and let's build something that works for your business.

Frequently asked questions

What is the simplest way for an SMB to start financial forecasting?

Start by analyzing your historical cash inflows and outflows, then project forward using a simple spreadsheet updated regularly. Build a cash flow forecast using an opening balance plus expected inflows and outflows for each period.

How often should I update my business forecasts?

Update your forecasts at least quarterly, but monthly reviews are best for fast-changing or cash-sensitive businesses. The GFOA forecasting framework treats monitoring and updating as core steps, not optional add-ons.

Why do my profit forecasts differ from cash flow?

Revenue and profit forecasts use accrual accounting, while cash flow reflects the real timing of money moving in and out, which usually lags behind recognized revenue. That timing gap is why profit and cash can diverge even in a strong quarter.

What is a scenario-based forecast and why use it?

A scenario-based forecast builds multiple "what-if" cases so your business can prepare for upsides and downsides, not just one expected outcome. Scenario forecasting quantifies coherent alternatives instead of claiming one certain answer.

How detailed should forecasted financials be for a small business?

In year one, forecast monthly; years two and three, quarterly; annual forecasts work for years four and beyond. SMB financial projections follow this structure to keep detail where it matters most without overcomplicating long-range planning.