Most business owners treat their annual financial statements like a final report card, reviewing the numbers once a year and hoping the grade is passing. But by the time those year-end figures arrive, the opportunities you missed or the cash flow problems that quietly grew are already history. Management accounts change that equation entirely. They give you a live, customizable window into your business's financial health throughout the year, so you can act on what's happening now, not what happened twelve months ago.

Table of Contents

- What are management accounts?

- How management accounts differ from statutory financial statements

- What goes into a typical set of management accounts?

- How to use management accounts for better business decisions

- Best practices for creating and interpreting management accounts

- Why flexible management accounts matter more than perfect templates

- Unlock the full value of management accounts with expert guidance

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Internal decision tool | Management accounts are tailored reports for owners and managers to steer the business, not for regulators or external parties. |

| Flexible and timely | They are produced as often as needed, delivering up-to-date insights that go beyond annual statutory reports. |

| Strategic value | Effective use of management accounts enables faster response to changes and supports smarter, data-driven decisions. |

| No one-size-fits-all | The format and focus of management accounts should match your business’s unique needs, not external templates. |

What are management accounts?

Management accounts are financial reports built specifically for the people running your business. Unlike the formal statements you file with tax authorities or share with outside investors, these reports exist purely to help you and your team make better decisions, faster.

As the ICAEW explains, "management accounts are internal financial reports prepared regularly (typically monthly or quarterly) to help owners and managers monitor performance and make decisions during the year." That regularity is what sets them apart. Instead of waiting for year-end, you get a consistent pulse check on your business.

The content of management accounts is entirely up to you. There are no external frameworks like GAAP or IFRS dictating what must be included or how it must be formatted. You can build reports around whatever your business actually needs to track, whether that is departmental profitability, cash runway, sales performance by region, or inventory turnover rates.

Here are the core characteristics that define management accounts:

- Prepared for internal use only, not for regulators, banks, or tax authorities

- Produced on a regular schedule, typically monthly or quarterly, sometimes in real time

- Fully customizable to reflect the priorities and structure of your specific business

- Forward-looking as well as historical, often including forecasts and budget comparisons

- Not bound by external accounting standards, giving you total flexibility in format and content

Strong accounting and bookkeeping practices form the foundation of reliable management accounts. If your underlying financial data is messy or delayed, your management reports will reflect that, and the decisions you make based on them will suffer.

"Management accounts are not about compliance. They are about clarity. When they are done well, they tell you exactly where your business stands and where it is headed."

Think of management accounts as the dashboard of your business. Your statutory accounts are the maintenance log stored in the glove compartment. Both matter, but one tells you what is happening right now, and the other tells you what happened in the past.

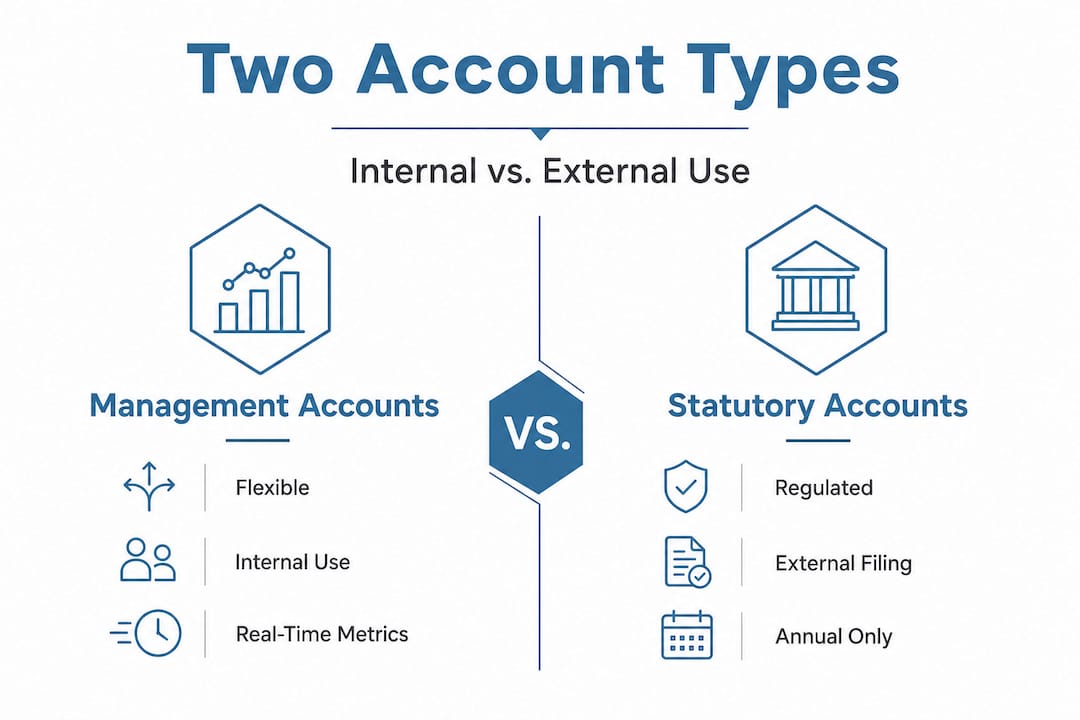

How management accounts differ from statutory financial statements

Understanding the difference between management accounts and statutory accounts is essential before you can use either effectively. They serve completely different audiences and answer completely different questions.

Statutory accounts are a legal requirement. Every incorporated business must produce them annually, following strict formatting rules and accounting standards. They are designed for external audiences: investors, lenders, regulators, and tax authorities. They are historical by nature, reflecting what happened during a completed financial year.

Management accounts, by contrast, are entirely internal. As ICAEW's career resources note, "management accounting is for internal stakeholders, tailored to decision needs, and not bound by formal external standards like IFRS/GAAP." That freedom is a feature, not a gap.

Here is a direct comparison to make the distinction concrete:

| Feature | Management accounts | Statutory accounts |

|---|---|---|

| Audience | Internal managers and owners | External regulators, investors, lenders |

| Frequency | Monthly, quarterly, or real time | Annually |

| Format | Fully customizable | Governed by GAAP/IFRS standards |

| Purpose | Operational and strategic decisions | Legal compliance and external reporting |

| Time orientation | Current and forward-looking | Historical |

| Legal requirement | No | Yes |

| Level of detail | As granular as needed | Standardized summary format |

The critical takeaway here is that you need both, but for entirely different reasons. Your statutory accounts prove your business is compliant and financially legitimate. Your management accounts tell you whether your business is actually performing well and where to focus your energy next month.

Pro Tip: If you find yourself making major business decisions based only on your annual statutory accounts, you are essentially driving by looking in the rearview mirror. Monthly management accounts give you the windshield view.

What goes into a typical set of management accounts?

Management accounts are flexible by design, but most well-structured sets share a common core of components. The specific mix depends on your industry, business model, and what decisions your leadership team needs to make regularly.

Here is what a typical set of management accounts includes:

| Component | What it shows | Why it matters |

|---|---|---|

| Summary profit and loss (P&L) | Revenue, costs, and net profit for the period | Tracks whether the business is generating profit |

| Cash flow statement | Cash coming in and going out | Prevents cash shortfalls before they happen |

| Budget vs. actuals | Planned figures compared to real results | Highlights where performance is ahead or behind |

| Balance sheet snapshot | Assets, liabilities, and equity at a point in time | Shows the overall financial position |

| Key performance indicators (KPIs) | Metrics specific to your business goals | Connects financial data to operational performance |

| Departmental or product breakdowns | Performance by team, region, or product line | Identifies what is working and what is not |

| Management commentary | Written narrative explaining key variances | Provides context that numbers alone cannot give |

Beyond the financial figures, many businesses include non-financial metrics in their management accounts. Sales pipeline data, customer acquisition costs, employee utilization rates, and inventory turnover can all appear alongside the numbers, giving a fuller picture of business health.

Management accounts are most useful when they deliver timely insights updated monthly or even in real time, focused on areas like profit and loss, cash flow, and operational KPIs. Timeliness is not optional here. A management account delivered six weeks after the period it covers has already lost most of its decision-making value.

The right operational efficiency audits can help you identify which metrics belong in your management accounts and which ones are just noise. Similarly, building a strong financial management and planning process ensures your management accounts feed directly into your broader business strategy rather than sitting as standalone reports.

One often-overlooked element is the management commentary. Numbers tell you what happened. Commentary tells you why it happened and what you plan to do about it. A well-written paragraph explaining a 15% revenue drop in a specific product line is worth more than a color-coded spreadsheet with no context.

How to use management accounts for better business decisions

Knowing what management accounts contain is only half the story. The real value comes from how you use them. Here is a practical framework for turning monthly reports into better business outcomes.

1. Spot trends before they become problems

When you review management accounts monthly, you start to see patterns that annual reviews completely miss. A gradual increase in cost of goods sold over three months, a slow decline in gross margin, or a consistent gap between budgeted and actual revenue are all signals that need attention well before year-end. Management accounts are a critical tool for controlling profits and losses precisely because their timeliness and flexibility make them invaluable for day-to-day decisions.

2. Identify your most and least profitable areas

A summary P&L tells you whether the business is profitable overall. A segmented management account tells you which products, services, regions, or teams are driving that profit and which are dragging it down. This is where management accounts earn their keep. You might discover that 20% of your product lines generate 80% of your profit, or that one regional office consistently underperforms against budget.

3. Compare actuals to budget every single month

Budget vs. actuals analysis is one of the most powerful tools in management accounting. When you set a budget at the start of the year and then track performance against it monthly, variances become visible immediately. A 10% overspend in marketing one month is manageable. That same overspend compounding for six months before anyone notices is a serious problem.

4. Use cash flow data to make timing decisions

Cash flow statements in management accounts let you plan major expenditures, hiring decisions, and investments with confidence. Knowing that you will have a cash shortfall in 60 days gives you time to arrange a credit line, delay a purchase, or accelerate collections. Discovering that shortfall when it arrives gives you nothing but stress.

5. Drive accountability across your leadership team

When department heads receive monthly reports showing their team's performance against budget and KPIs, accountability becomes built into the process. Regular efficiency analysis conversations become easier because everyone is working from the same data. This is also where strategic management decisions get grounded in evidence rather than gut feeling.

Pro Tip: Schedule a fixed monthly meeting to review management accounts with your leadership team. Even 30 minutes of structured discussion around the numbers creates more alignment and faster decision-making than ad hoc financial reviews ever will.

Best practices for creating and interpreting management accounts

Building management accounts is one thing. Building management accounts that people actually use and act on is another challenge entirely. These best practices separate reports that gather dust from reports that drive results.

-

Keep reporting intervals consistent. Monthly is the gold standard for most businesses. Quarterly works for smaller operations with slower-moving financials. Whatever interval you choose, stick to it. Inconsistent reporting makes trend analysis impossible and signals that financial discipline is not a priority.

-

Only include metrics that actually matter. More data is not always better. A 40-page management report covering every conceivable metric will get skimmed or ignored. Focus on the five to ten indicators that most directly reflect your business's current priorities and challenges.

-

Involve your key managers in shaping the format. The people who will use these reports should have input into what they contain. A sales director needs different information than an operations manager. Tailoring sections to each audience increases the chance that the reports actually influence decisions.

-

Write commentary that tells the story. Numbers without context are just numbers. Every significant variance, whether positive or negative, deserves a brief written explanation. What caused the variance? Is it a one-time event or a trend? What action is being taken?

-

Review and update the report structure regularly. As management accounting's deliverables are inherently audience-driven, they should not be forced into a rigid historical structure. Your business evolves, and your management accounts should evolve with it. A metric that was critical 18 months ago may no longer be relevant today.

Working with a skilled business consulting partner can help you design a management accounting framework that fits your business rather than a generic template. Pairing that with rigorous efficiency and cost analysis ensures your reports highlight the cost drivers that most affect your bottom line.

Why flexible management accounts matter more than perfect templates

Here is something we have seen consistently across the businesses we work with: the companies that get the most value from management accounts are not the ones using the most sophisticated templates. They are the ones who have built reports around the questions they actually need to answer.

There is a temptation, especially when you are new to management accounting, to search for the "right" format. Plenty of templates exist online, and many of them are perfectly fine starting points. But a template built for a manufacturing company with 200 employees will not serve a 15-person professional services firm particularly well, and forcing your business into someone else's framework is a waste of the one major advantage management accounts offer: total flexibility.

The freedom from external rules is not just a technical detail. It is the entire point. When you are not constrained by IFRS or GAAP, you can build reports that answer the questions keeping you up at night. What is my real cash position after committed expenses? Which client accounts are profitable and which are costing me money to serve? Am I on track to hit my growth targets for the quarter?

We have also seen businesses over-engineer their management accounts to the point where producing them becomes a monthly burden rather than a monthly benefit. If your finance team spends three weeks building a report that takes 10 minutes to review, something has gone wrong. The goal is insight, not elegance.

The best management accounts we have helped businesses build started simple and grew more sophisticated over time as the team learned what information actually changed their decisions. That iterative approach, supported by the right fractional CFO services expertise, consistently produces better outcomes than any off-the-shelf template.

Unlock the full value of management accounts with expert guidance

Understanding management accounts is a strong first step. Putting them to work consistently, with the right structure and the right metrics for your specific business, is where the real financial clarity begins.

At AmCFO, we help business owners and finance managers build management accounting processes that actually drive decisions. Whether you need support designing your first set of reports, cleaning up your underlying financial data, or getting a fractional CFO perspective on what your numbers are telling you, we have the expertise to help. Our fractional CFO services are built around your business's real needs, and our business consulting team can help you turn monthly financial data into a genuine competitive advantage. Reach out to AmCFO today and start making decisions with confidence.

Frequently asked questions

Who prepares management accounts within a company?

Management accounts are usually prepared by finance managers, controllers, or in-house accountants, since they are internal financial reports designed to help owners and managers monitor performance. Smaller businesses often outsource this function to a fractional CFO or accounting firm.

How often should management accounts be produced?

Most businesses benefit from monthly management accounts, though some produce them quarterly or in real time. Typically monthly or quarterly reporting gives leadership teams enough frequency to catch trends and respond before small issues become large ones.

What's the main difference between management and statutory accounts?

Statutory accounts are formal, externally audited reports required by law, while management accounts are flexible and tailored for internal decision-making. Management accounting is for internal stakeholders and is not bound by formal external standards like IFRS or GAAP.

Are management accounts required by law?

No, management accounts are not a legal requirement for any business. However, management accounts are not regulated by external standards, which means you have complete freedom to build them in whatever way serves your business best, making them one of the most practical financial tools available to any owner or manager.