Most business owners assume financial modeling belongs to Wall Street analysts and corporate finance teams. That assumption costs real money. Financial modeling is one of the most practical tools available to any business owner who wants to make better decisions, plan for uncertainty, and understand where their company is actually headed. This guide breaks down the fundamentals, shows you how the core model structure works, explains scenario analysis in plain language, and highlights the expert-level nuances that can make or break your projections.

Table of Contents

- What is financial modeling? The fundamentals explained

- Three-statement models: The backbone of effective financial modeling

- Scenario analysis and sensitivity testing: Exploring business "what ifs"

- Model structure and auditability: Keys to reliable financial models

- Expert modeling nuances: Real vs. nominal assumptions in business valuations

- What most guides miss about financial modeling for business owners

- Take your financial modeling to the next level

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Clear definition | Financial modeling organizes business data and assumptions into projections that aid decision-making. |

| Three-statement model | Linking income, balance sheet, and cash flow statements enables consistent and insightful analysis. |

| Scenario-driven insight | Testing different assumptions reveals risks, opportunities, and supports more informed planning. |

| Best practice structure | Separating inputs, historicals, and calculations helps reduce errors and build reliable models. |

| Advanced nuances | Consistency between real and nominal assumptions is essential for accurate business valuations. |

What is financial modeling? The fundamentals explained

Financial modeling is not just a spreadsheet with revenue projections. It is a structured way of translating your business assumptions into numbers that tell a story about the future.

"Financial modeling is the process of building a structured representation of a company's past, current, and projected financial performance using historical data and forward-looking assumptions, to support decision-making and (often) valuation." — Wall Street Prep

That definition matters because it separates modeling from casual forecasting. A forecast might say, "We expect $2 million in revenue next year." A financial model asks: Why $2 million? What pricing, volume, headcount, and margin assumptions produce that number? And what happens if any of those assumptions shift?

Business assumptions are the raw material of any model. Common examples include:

- Pricing: If you raise your service fee by 10%, how does that flow through to gross margin?

- Volume: If you close 20% fewer clients in Q2, what does cash flow look like in Q3?

- Headcount: If you add two salespeople, when does the revenue they generate cover their cost?

- Margins: If supplier costs increase by 8%, at what point does profitability erode below your target?

- Capital expenditures (CapEx): If you buy new equipment this year, how does depreciation affect taxable income over the next five years?

These are not abstract finance questions. They are the exact questions business owners face every month. A financial model gives you a structured, quantified way to answer them before you commit to a decision. Our business consulting insights explore how modeling supports strategic planning at every stage of growth.

One important distinction: modeling is not the same as sales forecasting for business growth. Forecasting typically produces a single expected outcome. Modeling builds the machinery that lets you test dozens of outcomes quickly, with every assumption visible and adjustable.

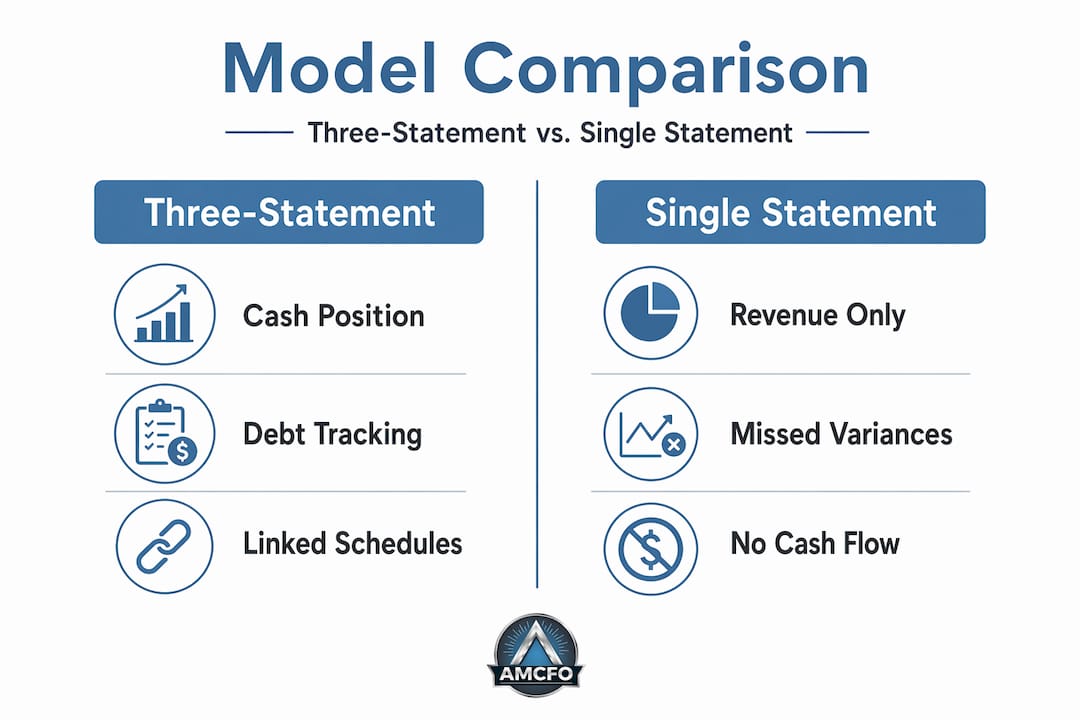

Three-statement models: The backbone of effective financial modeling

Having defined what financial modeling is, it is essential to understand its core structure. Most serious financial models are built around three financial statements working together.

"A central methodology in corporate financial modeling is the three-statement (3-statement) model, which links the income statement, balance sheet, and cash flow statement so changes in assumptions flow consistently through all outputs." — Valuation Master Class

Here is how the three statements relate to each other:

- Income statement: Records revenue, expenses, and net profit for a period. This is where your pricing and volume assumptions hit first.

- Balance sheet: Shows what the company owns and owes at a point in time. Net income from the income statement flows into retained earnings on the balance sheet.

- Cash flow statement: Reconciles net income with actual cash movement. Non-cash items like depreciation and changes in working capital adjust the income statement figure to show real liquidity.

When these three are linked properly, changing one assumption ripples through all three statements automatically. Here is a numbered example of how that works in practice:

- You increase prices by 8%, raising revenue on the income statement.

- Higher revenue increases net income, which flows to retained earnings on the balance sheet.

- The cash flow statement reflects the increased cash from operations, adjusted for any changes in accounts receivable if customers pay on credit terms.

- The balance sheet now shows higher cash and equity, which affects your debt-to-equity ratio.

- That ratio change might affect your borrowing capacity, which feeds back into future CapEx planning.

That chain reaction is why a single-statement analysis is so limited. Looking only at your income statement tells you whether you made money. The three-statement model tells you whether you have money, whether you can grow, and whether you can survive a bad quarter.

| Feature | Three-statement model | Single-statement analysis |

|---|---|---|

| Captures cash position | Yes | No |

| Links profit to liquidity | Yes | No |

| Supports valuation work | Yes | Rarely |

| Reveals working capital gaps | Yes | No |

| Useful for lender presentations | Yes | Limited |

| Complexity level | Moderate to high | Low |

For executives thinking about long-term planning, strategic management modeling provides a framework for connecting these financial outputs to operational goals. Tools designed for revenue forecasting can also feed directly into the income statement layer of your three-statement model.

Scenario analysis and sensitivity testing: Exploring business "what ifs"

Understanding the linked statements sets the stage for evaluating different business scenarios. This is where financial modeling shifts from descriptive to genuinely strategic.

Scenario analysis and sensitivity testing move modeling beyond a single point forecast. Instead of asking "what will happen," you ask "what could happen under a range of conditions." That shift in framing changes how you make decisions.

Common scenarios that business owners should model include:

- Price increase scenario: What happens to margin and customer retention if you raise prices by 5%, 10%, or 15%?

- Cost reduction scenario: If you renegotiate a supplier contract and cut COGS by 6%, how quickly does that improve operating cash flow?

- Volume fluctuation: What does a 20% drop in new client acquisitions do to your 12-month runway?

- Hiring scenario: If you bring on a department head at $120,000 per year, at what revenue level does that investment break even?

- Economic downturn scenario: If your top three clients reduce spending by 30%, can you cover fixed costs for six months without new financing?

Sensitivity testing is a related but slightly different tool. Where scenario analysis changes multiple assumptions at once to create a full picture, sensitivity testing isolates one variable at a time. You might test how net income changes as gross margin moves from 40% to 60% in 5% increments, holding everything else constant. This reveals which assumptions your model is most sensitive to, and therefore which business levers deserve the most attention.

Pro Tip: Always stress test your model with a "worst case" scenario that feels uncomfortably pessimistic. If the business can survive that scenario, you have real confidence. If it cannot, you have critical information before it becomes a crisis.

Our efficiency analysis services help businesses identify which operational variables to prioritize in scenario testing. For a deeper look at sales forecasting approaches, external resources can help you build the revenue assumptions that feed your scenarios.

The value of scenario modeling over a single forecast is not just intellectual. It forces you to articulate your assumptions explicitly, which makes them visible, debatable, and improvable. Many business owners discover through this process that their "optimistic" base case was actually built on assumptions that had never been questioned.

Model structure and auditability: Keys to reliable financial models

With scenario modeling in mind, the reliability of your projections depends on how well your model is structured and maintained. A technically sophisticated model built on a messy foundation is worse than a simple model built cleanly.

Best-practice model structure separates inputs (your drivers and assumptions) from historical data and from the calculations and outputs. This separation sounds simple, but most business models violate it constantly. When assumptions are buried inside formulas, no one can audit them. When historical data is mixed with projections in the same cells, errors become invisible.

Common expert-level failure modes include silent data and logic issues such as mixing sign conventions, missing time-period alignment between schedules, inadequate error checks, and insufficient stress-testing. These are not beginner mistakes. They show up in models built by experienced people who are moving too fast.

| Best practice element | Common pitfall |

|---|---|

| Dedicated input tab with labeled assumptions | Assumptions hardcoded inside formulas |

| Consistent sign conventions throughout | Mixing positive and negative conventions by section |

| Time-period alignment across all schedules | Mismatched monthly vs. annual periods in linked sheets |

| Built-in error checks (balance sheet balances, etc.) | No validation formulas |

| Clear version control and change log | Overwritten files with no history |

| Regular stress-testing cadence | Model tested once at build, never revisited |

A real-world example: a mid-sized distribution company built a model to evaluate a warehouse expansion. The model looked professional. But one input cell, the cost per square foot, was entered as a positive number in one section and a negative in another. The error was silent. The model showed the expansion as profitable. The company committed $800,000. Six months later, the actual financials revealed the project was underwater from day one. The model had not been audited.

Pro Tip: Before presenting any model to a lender, investor, or board, run a simple checklist: Does the balance sheet balance? Do cash flows reconcile? Are all input assumptions visible on a single tab? Can someone unfamiliar with the model understand it in 15 minutes? If the answer to any of these is no, the model is not ready.

Our strategic growth consulting team works with businesses to build model structures that hold up under scrutiny. Pairing that with solid financial planning support ensures your projections are grounded in real operational data. For additional context, sales modeling best practices offer useful structural guidance for the revenue side of your model.

Expert modeling nuances: Real vs. nominal assumptions in business valuations

After mastering basic structure and reliability, it is pivotal to recognize advanced modeling nuances that can impact your business valuation outcomes. One of the most commonly mishandled issues involves real versus nominal assumptions.

Here is the plain-language version: nominal figures include inflation. Real figures strip inflation out. A cash flow projection that grows at 5% per year in nominal terms is only growing at roughly 2% in real terms if inflation is running at 3%. This distinction matters enormously in discounted cash flow (DCF) models, which are used to value businesses for acquisitions, investor presentations, and exit planning.

"DCF models must be internally consistent about real vs. nominal assumptions (cash flows vs. discount rates and terminal growth). Mixing them can distort valuation." — Financial-Modeling.com

Common mistakes and their consequences include:

- Using nominal cash flows with a real discount rate: This overstates the present value of future cash flows, making the business appear more valuable than it is.

- Using a real terminal growth rate with nominal cash flows: This compounds the inflation error at the point where terminal value has the most weight in the total valuation.

- Inconsistent treatment across divisions: If one business unit is modeled in real terms and another in nominal terms, the consolidated model produces nonsense.

- Not documenting the convention used: Even if the model is internally consistent, an undocumented convention creates confusion for anyone reviewing or updating it later.

As an executive, you do not need to build these models yourself. But you do need to ask the right questions. When a consultant or CFO presents a valuation, ask: "Are these cash flows real or nominal? Is the discount rate consistent with that choice? What inflation assumption is embedded in the terminal growth rate?" Those three questions will immediately reveal whether the model has been built with rigor or with speed.

Our fractional CFO services include valuation support that addresses exactly these consistency issues. For client acquisition modeling, consistent assumptions across your revenue and cost projections are equally important.

What most guides miss about financial modeling for business owners

Most financial modeling guides focus on technical structure. They explain three-statement models, walk through DCF mechanics, and list best practices for spreadsheet hygiene. That content is useful. But it misses the deeper reason why financial models fail in real business environments.

Models fail when they are disconnected from the people running the business. A technically perfect model built by a consultant who spent two days on-site will underperform a simpler model built by someone who understands why the business actually makes money. The assumptions are only as good as the business knowledge behind them.

Here is the contrarian view we have developed through working with businesses across industries: auditability matters more than sophistication. A model that a non-finance executive can open, understand, and challenge is more valuable than a complex model that only one person can interpret. Complexity without transparency is not rigor. It is a liability.

The hard-won lesson is about maintenance. Most businesses build a model for a specific purpose, use it once, and let it go stale. Then, 18 months later, someone dusts it off, updates two cells, and presents it as current analysis. The underlying assumptions may be completely obsolete. Regular model updates and stress-tests are not optional housekeeping tasks. They are the difference between a model that guides decisions and one that creates false confidence.

What should executives demand from their finance teams and consultants? First, every model should have a visible assumption log that gets reviewed quarterly. Second, every major decision should be stress-tested against a scenario that the team genuinely hopes will not happen. Third, any model used for valuation or capital allocation should be reviewed by someone who did not build it. Our forensic accounting work frequently uncovers modeling errors that went undetected for years because no independent review was ever performed.

The businesses that use financial modeling most effectively treat it as a living management tool, not a one-time deliverable. That mindset shift is worth more than any technical upgrade.

Take your financial modeling to the next level

After exploring what matters most in financial modeling for business owners, the next step is connecting those insights to expert support that fits your business.

At AmCFO, we work with business owners and executives who want financial clarity without the overhead of a full-time CFO. Our fractional CFO services include financial modeling, scenario analysis, and ongoing strategic guidance tailored to your industry and goals. Whether you need a three-statement model built from scratch, a valuation model reviewed for consistency, or financial planning support that connects your projections to real operational decisions, our team brings the expertise and transparency that serious business decisions require. Reach out to learn how we can help you model your next move with confidence.

Frequently asked questions

What is the main difference between financial modeling and financial forecasting?

Financial forecasting predicts the most likely outcome, while financial modeling evaluates hypothetical scenarios and tests "what-if" situations across a range of assumptions.

Why do financial models need to separate inputs from calculations and outputs?

Separating inputs from calculations keeps models auditable, easier to update, and far less prone to hidden errors that can silently distort your projections.

What are common mistakes business owners make in financial modeling?

Common expert-level failure modes include mixing sign conventions, misaligning time periods across schedules, skipping validation checks, and neglecting regular stress-testing.

How can scenario analysis improve my business decisions?

Scenario analysis evaluates how outcomes change under different assumptions, helping you plan for both risks and opportunities before committing resources.

Why does mixing real and nominal assumptions lead to faulty business valuations?

Mixing real and nominal assumptions invalidates the internal logic of a DCF model and can materially distort terminal values, leading to significant valuation errors.