You finish a strong quarter, invoices are out, and your income statement looks great. Then your bank account tells a completely different story. This disconnect happens to small business owners every day, and the accounting method you choose is often the reason. Cash and accrual accounting each show you a different version of your financial reality, and picking the wrong one can leave you underprepared for taxes, unable to secure financing, or blindsided by cash crunches. This guide breaks down both methods, helps you decide which one fits your situation, and walks you through exactly how to put it into practice.

Table of Contents

- Understanding cash vs. accrual accounting

- Which accounting method fits your business?

- Step-by-step: How to select and implement your accounting method

- Common mistakes and troubleshooting tips

- Why conventional advice on accounting methods misses the real business impact

- Get expert help choosing your accounting method

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Know your options | Small business owners must understand cash and accrual accounting before making a decision. |

| Assess eligibility | Use gross receipts and business complexity to decide which method fits your needs and IRS requirements. |

| Follow the right steps | Formal IRS procedures are required for changing accounting methods, especially as your business grows. |

| Prioritize accuracy | Accrual accounting provides more precise period reporting, particularly if your business handles credit sales or purchases. |

| Review annually | Revisit your accounting method each year to stay compliant and adapt to evolving business realities. |

Understanding cash vs. accrual accounting

Now that you know why the choice matters, let's break down what cash and accrual accounting actually mean.

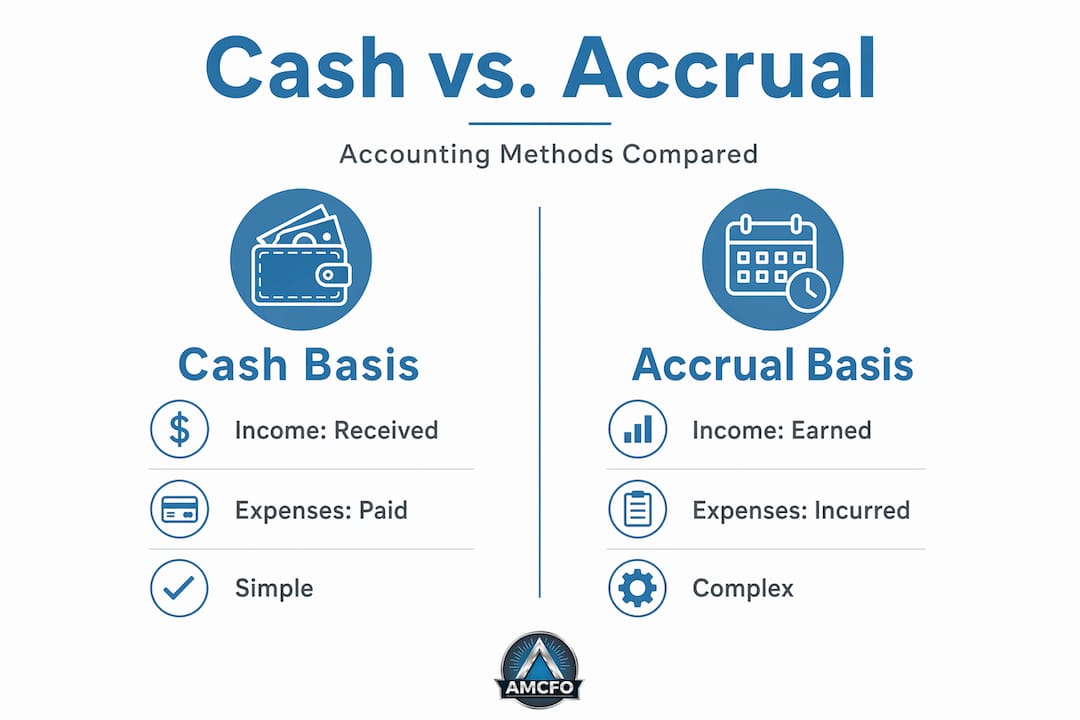

At its most basic, the difference comes down to timing. Cash basis records income when received and expenses when paid. Accrual recognizes income when earned and expenses when incurred. Those two sentences sound simple, but the downstream effects on your financial statements, tax obligations, and business decisions are significant.

Here's a concrete example. Imagine you complete a $10,000 consulting project in November and send the invoice. Your client pays in January. Under cash basis, that $10,000 lands in your January income. Under accrual, it shows up in November, the month you earned it. Neither is "wrong," but they tell very different stories. As SBA guidance describes, accrual records transactions when the sale is completed, while cash records when payment is received. That timing difference shapes every financial report you produce.

Pair that with our accounting and bookkeeping overview for context on how the method you choose affects every layer of your books.

Comparing the two methods at a glance

| Feature | Cash basis | Accrual basis |

|---|---|---|

| Revenue recognized | When cash is received | When earned |

| Expenses recognized | When cash is paid | When incurred |

| Complexity | Low | Higher |

| Financial visibility | Limited | More complete |

| Common users | Freelancers, sole proprietors | Growing businesses, those with credit terms |

| IRS eligibility | Under $25M avg. gross receipts | Required above threshold |

Which businesses tend to use each method?

Cash basis works well for:

- Freelancers and solo service providers with simple, transaction-based income

- Small retail operations that collect payment at the point of sale

- Businesses with no significant accounts receivable or payable balances

- Startups still figuring out their revenue patterns

Accrual basis fits better for:

- Businesses that extend credit to customers or receive goods on net payment terms

- Companies with significant inventory

- Any business seeking outside financing or investors, since lenders expect accrual-based statements

- Operations with complex revenue cycles, like subscription models or long-term contracts

If your business sits anywhere between these two profiles, consulting business consulting advice from a financial professional can help you read the nuances of your specific situation. Some industries, like cannabis and specialty retail, have additional considerations covered in detailed accrual accounting guides that go deeper into sector-specific compliance.

Which accounting method fits your business?

With a clear understanding of the two methods, let's figure out which fits your business best.

The IRS does not give every business a free choice. Eligibility for cash method is tied to an inflation-adjusted gross receipts threshold for federal tax purposes, generally $25 million or less average annual gross receipts over three years. If your revenue exceeds that threshold, you are required to use accrual for federal income taxes. That's the regulatory floor. But inside the eligible range, you still have a real decision to make.

Here is how to work through it:

- Calculate your average gross receipts. Add up your gross receipts for the last three tax years and divide by three. If you are under $25 million, cash basis is still available to you.

- Assess how much credit your business extends. Do you send invoices and wait 30, 60, or 90 days for payment? If yes, cash basis will consistently understate your earned income during the period you actually performed the work.

- Look at your payables. Do you receive inventory or services on credit before paying? Accrual matches those costs to the revenue they help generate, giving you truer margin data.

- Consider your reporting audience. Banks, investors, and sophisticated buyers expect accrual-based financial statements. If growth or financing is in your plans, accrual builds a stronger foundation now.

- Evaluate your internal capacity. Accrual requires more bookkeeping discipline. If you are just starting out and have no dedicated accounting support, cash basis may reduce errors in the short term.

"Businesses with credit terms may get less accurate period performance using cash basis, which can delay recognition." — Bank of America Cash vs. Accrual Guide

That quote captures a real risk. If you collect a large payment in March for work done in January and February, your March reports look inflated while January and February look lean. Over time, this distortion makes trend analysis unreliable. It also complicates month-over-month comparisons that are essential for spotting problems early.

Pro Tip: Match your accounting periods to how your business actually earns money. If you bill in cycles or on project milestones, accrual accounting lets your income statement reflect the real performance of each period rather than the luck of when checks arrive.

Running an efficiency and cost analysis is much more useful when your books reflect actual earning periods. Otherwise, you risk drawing conclusions from data that is off by weeks or months. Businesses that work through business process optimization often find that switching to accrual is part of getting their operational data to align with their financial data.

If managing this in-house feels like a stretch, many small businesses benefit from outsourcing accounting services to professionals who already know the technical requirements inside and out.

Step-by-step: How to select and implement your accounting method

Once you've decided which method is right, here's how to actually select and activate it.

The mechanics of switching or formalizing your method are not just internal bookkeeping decisions. IRS rules under IRC §446 and Revenue Procedure 2025-23 govern changes in accounting method for federal tax purposes. Changing your method without following those procedures can result in penalties, interest, and required adjustments that cost far more than getting it right the first time.

Implementation steps:

- Confirm your eligibility and current method. Pull your last three years of tax returns. Check how income was reported and whether it aligns with cash or accrual.

- Decide on the method going forward. Document your reasoning in writing, especially if you are switching. This record protects you during an audit.

- File Form 3115 if changing methods. Revenue Procedure 2025-23 outlines when automatic consent applies versus when you need advance IRS approval. Many method changes qualify for automatic consent, but the form is still required.

- Update your accounting software. QuickBooks lets users choose cash or accrual for their reports, which affects how transactions are displayed and how financial statements are generated.

- Reconcile any transition-year adjustments. When switching from cash to accrual, you may need to add outstanding receivables and payables to your books. Work with an accountant to handle this correctly so income is not double-counted or missed.

- Train your team. Anyone entering transactions needs to understand the new recognition rules. A single misentered invoice date can throw off your period reporting.

| Action item | Responsible party | Key document |

|---|---|---|

| Confirm eligibility | Business owner or CPA | Prior year tax returns |

| Document method choice | Accountant | Internal policy memo |

| File Form 3115 | CPA or tax advisor | IRS Form 3115 |

| Update software settings | Bookkeeper | QuickBooks preferences |

| Adjust opening balances | Accountant | Transition-year workpapers |

| Train staff | Operations lead | Procedures checklist |

Pro Tip: Set a calendar reminder to review your accounting method eligibility every year when you wrap up your books. Revenue growth can push you past the $25 million threshold faster than you expect, and missing the required transition is a compliance risk you do not want.

Running efficiency audits annually pairs naturally with this review. And if your business is scaling, a solid financial management and planning framework should include method eligibility as a standing checkpoint.

Common mistakes and troubleshooting tips

Even with a clear choice and implementation plan, mistakes can slip through. Let's look at how to avoid them.

The most common error small business owners make is treating a software setting change as a full method change. Toggling your reporting preference in QuickBooks does not satisfy IRS requirements. The underlying transaction data, the tax forms you file, and the formal election or change request all have to align. Getting this wrong can mean years of mismatched records that are expensive to untangle.

Mistakes to watch for and how to fix them:

- Changing software settings without filing Form 3115. Fix: Work with your CPA to determine if you need automatic consent or advance approval, then file the form before the due date.

- Not tracking gross receipts as you grow. Fix: Build a quarterly gross receipts review into your bookkeeping routine so you know where you stand relative to the $25 million threshold.

- Using cash basis while extending significant credit. Fix: If more than 20 to 30 percent of your revenue comes from invoiced sales with net terms, strongly consider switching to accrual to get accurate period data.

- Failing to adjust opening balances at transition. Fix: Have your accountant prepare a transition-year schedule that brings all outstanding receivables, payables, and prepaid items onto the balance sheet.

- Mixing methods across different parts of the business. Fix: Choose one method and apply it consistently. Hybrid methods exist under tax law but have strict rules, and applying them without guidance creates audit exposure.

If your business grows past eligibility for cash basis or becomes required to use accrual, you must follow IRS procedures to change methods. That is not optional, and the penalties for non-compliance are real.

Pro Tip: Every January, pull your rolling three-year average gross receipts. If you are approaching $20 million, start the accrual transition conversation with your accountant now, not after you cross the line.

Strategic growth consulting becomes particularly valuable at these inflection points, when your business is growing fast enough to trigger new compliance obligations. And if something has gone sideways with prior year reporting, forensic accounting guidance can help you reconstruct accurate records before problems compound.

Why conventional advice on accounting methods misses the real business impact

Most guides on this topic frame the cash versus accrual decision as a simplicity trade-off. Cash is easy. Accrual is complicated. Pick based on your tolerance for paperwork. That framing misses the deeper point entirely.

Your accounting method is not just a compliance checkbox. It is the lens through which you see your entire business. When you look at financial planning perspectives, the quality of those plans depends directly on whether your underlying financial data reflects reality.

Here is what conventional advice ignores. Businesses that operate on cash basis often make growth decisions based on distorted data. They think a month was profitable because three large payments happened to land. They think expenses are under control because a big vendor payment hasn't cleared yet. This is not financial management. It is financial storytelling with delayed punchlines.

Accrual accounting, for all its added complexity, forces discipline. You have to know what you've earned versus what you've collected. You have to recognize costs when you incur them. That discipline pays off when you go to budget for next year, evaluate a product line's true margin, or present financials to a bank. Businesses in other markets already understand this. International accounting examples show how entrepreneurs in structured economies use accrual principles to make sharper operational decisions, not just for compliance, but for genuine visibility.

The contrarian truth is this: if your business is growing and you are still on cash basis because it feels easier, you are paying a real cost in clarity. Every month you operate without period-matched financials is a month where your decisions are based on cash flow timing rather than actual business performance. Those are two very different things.

Get expert help choosing your accounting method

Choosing between cash and accrual accounting is not just a tax question. It affects how clearly you see your business, how confidently you plan, and how credibly you present your financials to lenders or partners.

At AmCFO, we bring fractional CFO expertise to small and mid-sized businesses that need accurate, strategic financial management without the cost of a full-time hire. Whether you need help selecting the right method from the start, managing a compliant transition, or cleaning up books that have gotten off track, our accounting and bookkeeping services are built to handle the technical work while keeping you in control of the decisions. Explore the full range of business finance solutions we offer and find the right support level for where your business is right now.

Frequently asked questions

Can I switch between cash and accrual accounting any time?

No. Changing methods for tax reporting requires IRS approval and formal procedures under Rev. Proc. 2025-23, not just a software setting change. Most switches require filing Form 3115 with your tax return.

Does QuickBooks let me report using either method?

Yes, QuickBooks users can choose cash or accrual for reporting purposes, but this reporting toggle does not replace your official IRS method election or satisfy formal change procedures.

What happens if my business outgrows the cash basis eligibility?

You must switch to accrual and follow IRS guidance for method changes, including formal application via Form 3115 and required balance sheet adjustments for the transition year.

How do credit terms affect my choice of accounting method?

If your business relies on credit sales or net-term purchases, accrual accounting offers more accurate period reporting because it matches income and expenses to the period they actually occurred, not when cash changes hands.