Strategic budget alignment is the practice of directing every dollar of organizational spending toward a defined, prioritized goal. Without this discipline, budgets become historical artifacts: last year's numbers plus a percentage increase, with no connection to where the organization actually needs to go. The industry term for this practice is strategic budgeting, and it functions as a governance mechanism, not just an expense control tool. Strategic budgeting is a long-range process that ensures multi-year initiatives receive consistent funding, avoiding premature cuts due to short-term pressures. Finance leaders who align budget with strategic goals convert their annual budget cycle into a forward-looking control system that enforces priorities across every department.

How to align budget with strategic goals: the foundation

The first requirement is strategic clarity before any numbers are entered. Effective strategic budgeting focuses on a 1–3 year horizon, with 40–60% of incremental investment prioritized for top strategic initiatives. That figure matters because it forces a real trade-off: if you commit the majority of new spending to your top three priorities, you cannot quietly fund everything else at the same time.

Before the budget process opens, finance teams need three things in place. First, leadership must agree on weighted strategic priorities, not just a list of goals but a ranked order with explicit relative importance. Second, cross-functional leaders must be in the room. Budget decisions made only inside finance produce numbers that operations, sales, and product teams immediately work around. Third, the organization needs a prioritization scorecard that scores each initiative on impact, confidence, time-to-value, and cash need.

The table below shows the core prerequisites and tools required before budget alignment work begins.

| Prerequisite | Tool or Method | Purpose |

|---|---|---|

| Weighted strategic priorities | Leadership ranking session | Forces explicit trade-offs before dollars are assigned |

| Cross-functional buy-in | Joint finance and operations workshops | Prevents budget workarounds at the department level |

| Initiative prioritization | Scorecard (impact, confidence, time-to-value, cash need) | Ranks initiatives objectively before funding decisions |

| Capital allocation criteria | Governance charter | Defines who approves what and at what threshold |

| Financial model per initiative | 12–24 month P&L projection | Connects each initiative to measurable financial outcomes |

Pro Tip: Run a one-day prioritization workshop with initiative owners before the budget template is ever opened. Decisions made in that room will save weeks of revision later.

How do you translate strategic objectives into budget line items?

Translating strategy into budget categories requires disaggregating each strategic pillar into financial drivers. A strategic goal like "expand into the mid-market segment" must become specific line items: sales headcount, marketing spend by channel, product development costs, and customer success capacity. Each line item needs a named strategic owner, not just a cost center code.

Finance teams must map material line items to strategic objectives and require justification of "Run the Business" versus "Grow the Business" spend during reviews. At least 20% of incremental budget is often allocated to growth initiatives. That distinction matters because it prevents operational maintenance costs from crowding out the investments that actually move the organization forward.

The most overlooked step is explicit defunding. Every budget cycle carries legacy spending: programs that were funded two years ago and never formally stopped. Alignment requires a deliberate decision to stop funding non-strategic items, not just to add new ones. Without that step, the budget grows in total size while strategic priorities receive only marginal new resources.

- Assign a named strategic owner to every material line item above a defined threshold.

- Require written justification for any line item that does not map to a current strategic priority.

- Separate "Run the Business" costs from "Grow the Business" costs in every department's budget submission.

- Flag legacy items for explicit review rather than automatic renewal.

- Link each growth initiative to at least one measurable KPI with a defined target and timeline.

Pro Tip: Create a "stop doing" list alongside the budget. Defunding non-strategic work is the fastest way to free capital for priorities without increasing total spend.

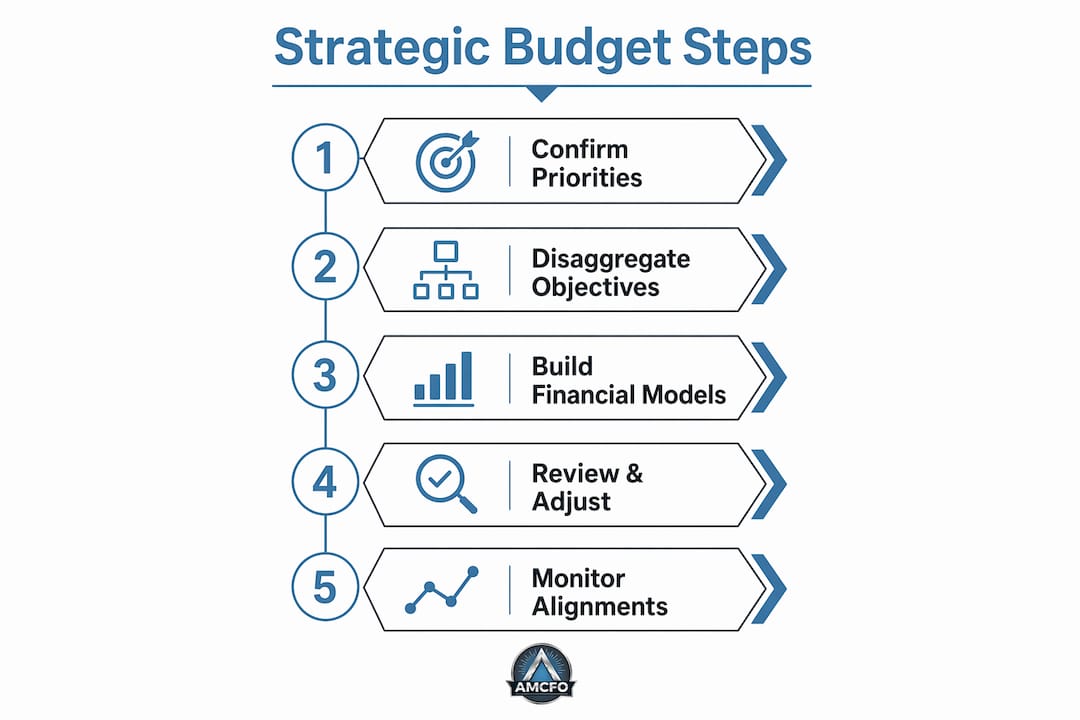

What are the key steps in building and reviewing a strategic budget?

Building a budget that stays connected to strategy requires a defined sequence. Skipping steps, especially the prioritization phase, produces a budget that looks strategic on paper but funds everything equally in practice.

- Confirm strategic priorities and weights. Leadership agrees on the top three to five initiatives and assigns relative importance before any financial modeling begins.

- Score and rank initiatives. Use a scorecard rubric covering impact, confidence, time-to-value, and cash need. Fund the top 40–60% of scored initiatives first.

- Build lean 12–24 month financial models. Each initiative gets its own P&L projection with at least two scenario variants: a base case and a downside. Financial modeling at the initiative level connects investment decisions to measurable outcomes.

- Set success gates. Success gates and KPIs should be defined to trigger accelerate, pause, or stop funding decisions, preventing sunk-cost bias. A gate is a predefined milestone: if the initiative hits it, funding continues; if it misses, leadership decides whether to adjust or stop.

- Embed quarterly reforecasting. Leading organizations use rolling strategic reviews with mandatory quarterly reforecasting to maintain budget-strategy alignment. Quarterly reviews prevent the budget from drifting out of sync with actual business conditions.

The table below shows how this process differs from a traditional annual budget cycle.

| Dimension | Traditional budgeting | Strategic budgeting |

|---|---|---|

| Time horizon | 12 months | 1–3 years with rolling updates |

| Starting point | Prior year actuals | Confirmed strategic priorities |

| Allocation logic | Incremental percentage increase | Weighted scoring and prioritization |

| Review frequency | Annual | Quarterly reforecast with success gates |

| Accountability | Cost center managers | Named strategic initiative owners |

Pro Tip: Build your financial models in layers: fixed operational costs first, then strategic initiative costs on top. This makes it immediately visible how much of the budget is discretionary versus committed.

How do you fix misalignment between budget and strategy over time?

The most common failure mode is reverse sequencing: finance builds the budget model before leadership has confirmed strategic priorities and weights. The result is a budget that reflects last year's organizational structure, not next year's strategic direction. Reverse sequencing undermines alignment and financial governance at the root level.

Equal fund distribution is the second major pitfall. When leadership cannot agree on priorities, the default is to give every department a similar percentage increase. CFOs must distinguish capital discipline from dynamic resource allocation to avoid equal fund distribution signaling weak governance. Spreading resources evenly signals that nothing is truly a priority, which fragments execution across the organization.

Silent carryover is the third failure. Funded initiatives that miss their success gates continue receiving resources because no one formally stops them. This is where sunk-cost bias does the most damage.

The budget is not a financial document. It is a statement of organizational intent. When every line item traces back to a confirmed priority, and every strategic owner is accountable for outcomes rather than just expenses, the budget becomes the most powerful governance tool a leadership team has.

Practical fixes for each failure mode:

- Reverse sequencing: Lock strategic priorities and weights before the budget template is distributed.

- Equal distribution: Require leadership to rank initiatives and document the rationale for each funding decision.

- Silent carryover: Review all active initiatives quarterly against their predefined success gates. Stop funding initiatives that miss two consecutive gates.

- Accountability gaps: Assign budget authority to the person responsible for the strategic outcome, not to the finance team alone.

The CFO advisory function plays a direct role here. A finance leader who surfaces these failure modes early, before the budget is finalized, saves the organization from funding the wrong priorities for an entire fiscal year.

Key Takeaways

Aligning budget with strategic goals requires confirmed priorities, initiative-level financial models, named accountability, and quarterly reviews to prevent drift.

| Point | Details |

|---|---|

| Confirm priorities first | Lock weighted strategic priorities before any financial modeling begins to avoid reverse sequencing. |

| Score and fund selectively | Use a prioritization scorecard and fund the top 40–60% of initiatives before allocating remaining resources. |

| Separate run vs. grow spend | Require explicit justification for "Run the Business" versus "Grow the Business" costs in every department. |

| Set success gates | Define predefined KPI milestones that trigger funding decisions to prevent sunk-cost bias. |

| Reforecast quarterly | Embed rolling quarterly reviews to keep the budget connected to actual strategic conditions. |

Budget alignment requires leadership, not just spreadsheets

I have worked with finance teams that built technically perfect budget models and still ended up funding the wrong things. The model was not the problem. The problem was that no one had the authority, or the willingness, to tell a department head that their project was not a priority this year.

Budget alignment is a leadership act before it is a financial one. The scorecard, the success gates, the quarterly reforecast: these are tools. They only work when a senior leader is willing to enforce the trade-offs they reveal. The organizations that do this well treat the budget as a live governance document, not an annual ritual. They revisit it when conditions change, reallocate capital when a gate is missed, and reward the leaders who flag problems early rather than hide them.

The most underrated practice I have seen is assigning a named strategic owner to every funded initiative. Not a cost center. Not a department. A person. When one person is accountable for both the spending and the outcome, the conversation in a quarterly review changes completely. It shifts from "why did we go over budget" to "are we on track to hit the goal we funded this for." That shift is where real strategic financial management begins.

— Angelica

Amcfo helps businesses connect budgets to strategy

Knowing the framework is one thing. Executing it without dedicated financial leadership is another challenge entirely.

Amcfo provides fractional CFO services built for exactly this kind of work: confirming strategic priorities, building initiative-level financial models, setting success gates, and running quarterly reforecasts. Business leaders get senior-level financial guidance without the cost of a full-time executive. Whether your organization needs a complete budget alignment process built from scratch or a review of an existing one, Amcfo's team brings the governance structure and financial modeling expertise to make it work. Explore Amcfo's full range of financial management services to find the right level of support for your goals.

FAQ

What does it mean to align budget with strategic goals?

Aligning budget with strategic goals means directing every material line item of spending toward a confirmed, weighted organizational priority. It transforms budgeting from an annual expense exercise into a governance mechanism that enforces strategic intent.

What is the difference between strategic budgeting and traditional budgeting?

Traditional budgeting starts from prior year actuals and applies incremental adjustments. Strategic budgeting starts from confirmed priorities, scores initiatives, and allocates resources based on strategic weight rather than historical patterns.

How often should a strategically aligned budget be reviewed?

Leading organizations conduct mandatory quarterly reforecasts to maintain alignment between the budget and current strategic conditions. Quarterly reviews allow leadership to adjust funding when success gates are missed or priorities shift.

What is a success gate in strategic budgeting?

A success gate is a predefined milestone or KPI that triggers a funding decision: accelerate, pause, or stop. Success gates prevent sunk-cost bias by requiring evidence of progress before continued investment is approved.

Why does equal fund distribution signal weak governance?

Equal fund distribution means leadership has not made explicit trade-offs between priorities. When every department receives a similar percentage increase, no initiative receives the concentrated resources needed to execute at the level the strategy requires.