Financial modeling is defined as the process of building dynamic, linked spreadsheet representations of a company's financial performance to project future revenue, expenses, and cash flows. The practice sits at the core of every serious business decision, from startup funding rounds to corporate acquisitions. A well-built model connects three core financial statements, the income statement, the balance sheet, and the cash flow statement, into one living document that updates when assumptions change. Understanding financial modeling basics gives analysts and business professionals the power to test ideas before committing capital, making it one of the most transferable skills in finance.

What are the essential components of a financial model?

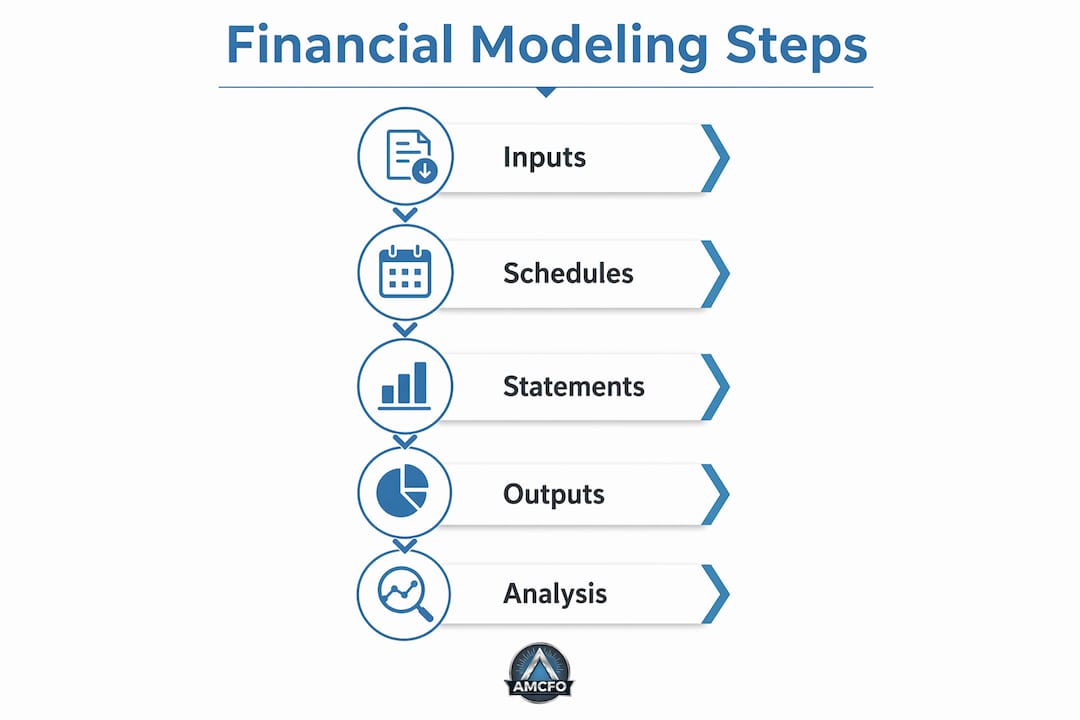

A financial model is built from four layers: inputs, supporting schedules, linked statements, and outputs. Each layer feeds the next, and a break at any point corrupts everything downstream. Models typically incorporate 3–5 years of historical income, balance sheet, and cash flow data as the baseline for projections. That history gives the model its credibility.

Inputs and assumptions

Inputs are the model's control room. They include revenue growth rates, operating margins, capital expenditure forecasts, and tax rates. Keeping all assumptions on a single, clearly labeled tab prevents the most common modeling error: hard-coding numbers directly into formulas. Hard-coded values make models brittle and nearly impossible to audit. Every number that can change should live in one place.

The three linked financial statements

The income statement drives net income, which flows into retained earnings on the balance sheet. The balance sheet's cash position ties directly to the cash flow statement. Dynamic linking of these three statements is non-negotiable. Static models that do not update automatically break model integrity the moment an assumption changes.

The ultimate test of a model's integrity is a balanced balance sheet. Assets must equal liabilities plus equity at every period. If the sheet does not balance, there is a broken link or a logic error somewhere in the model.

Outputs and key metrics

Outputs translate the model's calculations into decisions. The most common outputs are net present value (NPV), internal rate of return (IRR), and return on investment (ROI). Key outputs like NPV and IRR give executives a single number to compare against a hurdle rate or competing investment. Without clear outputs, a model is just a spreadsheet.

Pro Tip: Build a dedicated "dashboard" tab that pulls only the key outputs from your model. Executives rarely need to see every formula. They need the three numbers that drive the decision.

Which types of financial models are used most often?

Different business problems call for different model structures. A startup pitching to venture capital needs a different model than a private equity firm evaluating a leveraged buyout. The table below maps the most common model types to their typical use cases and users.

| Model type | Primary purpose | Typical users |

|---|---|---|

| Three-statement model | Integrated financial forecasting | Analysts, CFOs, lenders |

| DCF valuation model | Intrinsic business valuation | Investment bankers, acquirers |

| Budget and forecast model | Annual planning and variance tracking | FP&A teams, controllers |

| Scenario analysis model | Risk assessment across multiple outcomes | Strategy teams, consultants |

| LBO model | Leveraged acquisition analysis | Private equity professionals |

The three-statement model is the foundation for almost every other model type. Build it well, and the others become extensions of the same logic.

DCF valuation uses a free cash flow forecast, a terminal value, and a discount rate (WACC) to translate future cash flows into present value. It is the standard method for valuing a business during M&A transactions. The discount rate assumption alone can swing a valuation by millions of dollars, which is why analysts always run sensitivity tables around it.

Budget and forecast models serve a different purpose. They track actual performance against a plan and flag variances early. For most operating businesses, this is the model that gets used every single month. Scenario and sensitivity models layer on top of any base model to answer "what if" questions about growth, costs, or market conditions.

How does financial modeling support real business decisions?

Financial modeling is the tool that turns gut instinct into a testable hypothesis. Scenario and sensitivity analyses provide multiple outcome projections, covering best-case, worst-case, and base-case scenarios, so decision-makers can evaluate risk before committing. That structure forces discipline. You cannot hide a bad assumption inside a scenario table.

Here is how analysts apply these techniques in practice:

- Revenue sensitivity analysis. Change the revenue growth rate by 2% in either direction and observe the impact on operating cash flow and debt coverage. This single test reveals how much cushion the business actually has.

- Cost structure stress testing. Model a 15% increase in cost of goods sold to simulate supply chain pressure. Financial modeling simulates high-impact scenarios like supply chain disruptions rather than relying on intuition.

- Capital expenditure planning. Build a schedule that shows how a new equipment purchase affects depreciation, cash flow, and the balance sheet over five years. This gives the CFO a clear picture before signing a lease or loan.

- Investment evaluation. Run an IRR calculation on a proposed acquisition. If the IRR falls below the company's cost of capital, the deal does not create value at the assumed price.

- Annual budgeting. Use the prior year's three-statement model as the base. Adjust assumptions for the coming year and produce a monthly budget that the operations team can track against actuals.

Accurate, data-driven strategies require balancing historical data with critical thinking under real decision-making pressure. A model built in a vacuum, without input from operations, sales, or finance leadership, produces projections that no one trusts. The best models are built collaboratively. For a deeper look at applying these techniques, the practical guide for business owners covers how to connect model outputs directly to operating decisions.

Pro Tip: Always run your sensitivity analysis before presenting a model to leadership. Know which assumption moves the needle most. That is the assumption they will challenge first.

What are the most common financial modeling mistakes?

Most modeling errors are not math errors. They are structural errors that compound silently over time. Revenue growth assumption errors cascade through linked statements and produce wildly inaccurate long-term forecasts. A 1% misjudgment in year one becomes a multi-million dollar distortion by year five.

The most damaging mistakes analysts make:

- Hard-coding values in formulas. When a number changes, you cannot find every instance. The model breaks without warning.

- Broken statement linkages. Net income that does not flow to retained earnings, or cash that does not reconcile between the balance sheet and cash flow statement, destroys model integrity.

- Assumption errors left unvalidated. Growth rates, margins, and tax rates should always be benchmarked against industry data or historical performance before being locked in.

- No version control. Overwriting a working model with a broken update is a common and painful mistake. Save dated versions at every major revision.

- Circular references without resolution. Interest expense that depends on debt, which depends on cash, which depends on interest expense, creates a loop that crashes the model unless handled correctly.

Separating assumptions into dedicated input panels prevents most of these errors. When every assumption lives in one place, auditing the model takes minutes instead of hours. Debugging logical linkages should be the first step whenever a model produces unexpected results.

Pro Tip: Add a simple balance check formula at the top of your balance sheet tab: Assets minus Liabilities minus Equity equals zero. Color it red if the result is anything other than zero. You will catch errors instantly.

The business forecasting methods used by financial leaders reinforce the same principle: structure prevents error, and error prevention is faster than error correction.

Key Takeaways

A financial model's value comes from its structure, not its complexity. Linked statements, clean inputs, and validated assumptions are what separate a reliable model from a misleading one.

| Point | Details |

|---|---|

| Start with historical data | Use 3–5 years of income, balance sheet, and cash flow records as your projection baseline. |

| Separate inputs from formulas | Keep all assumptions on one tab to prevent hard-coding errors and simplify audits. |

| Link all three statements | Income statement, balance sheet, and cash flow must update dynamically or the model breaks. |

| Run scenario analysis | Test best-case, base-case, and worst-case outcomes before presenting any projection. |

| Validate with a balance check | A balanced balance sheet is the single most reliable test of model integrity. |

Financial modeling is a navigation tool, not a reporting exercise

I have reviewed hundreds of financial models built by analysts at every experience level, and the pattern is consistent: the most technically impressive models are often the least useful. Analysts spend weeks building elaborate structures with dozens of tabs, automated charts, and color-coded dashboards. Then a CFO asks one simple question, "What happens to cash flow if revenue drops 10%?" and the model cannot answer it cleanly.

Financial models are navigation systems rather than reporting tools. That distinction matters more than most analysts realize early in their careers. A navigation system is built to answer questions under pressure. A reporting tool is built to look good after the fact. The best models I have seen were simple, fast to update, and built around the three or four decisions the business actually needed to make.

Financial modeling mastery relies more on understanding how financial statements link together than on advanced math or software. I have watched analysts with basic Excel skills outperform colleagues with advanced certifications because they understood the logic of the income statement flowing into the balance sheet. Software changes. That logic does not.

The future of financial modeling will involve more automation and AI-assisted forecasting. But the analysts who will use those tools well are the ones who understand what the model is actually doing underneath the interface. Learn the fundamentals first. The tools will follow.

— Angelica

How Amcfo supports financial modeling and business planning

Amcfo works with businesses across industries to build the financial foundation that makes modeling possible in the first place. Accurate modeling starts with clean books, reliable historical data, and a clear picture of cash flow.

Amcfo's fractional CFO services bring CFO-level financial modeling expertise to businesses that do not need a full-time hire. The team builds forecasts, runs scenario analyses, and translates model outputs into decisions that leadership can act on. For businesses that need the underlying data cleaned up first, Amcfo's accounting and bookkeeping services organize the historical records that every reliable model depends on. Reach out to Amcfo to discuss what financial modeling support looks like for your business.

FAQ

What is financial modeling in simple terms?

Financial modeling is the process of building a linked spreadsheet that represents a company's financial performance and projects future revenue, expenses, and cash flows. It connects the income statement, balance sheet, and cash flow statement into one dynamic document.

What are the three core financial statements in a model?

The three core statements are the income statement, the balance sheet, and the cash flow statement. They must be dynamically linked so that a change in one assumption automatically updates all three.

How do scenario and sensitivity analyses work in financial modeling?

Scenario analysis tests best-case, base-case, and worst-case outcomes by changing key assumptions. Sensitivity analysis isolates one variable at a time to show how much it moves the final result, such as cash flow or valuation.

What is the most common financial modeling mistake?

Hard-coding values directly into formulas is the most damaging error. It makes models impossible to audit and causes silent errors when assumptions change. All inputs should live on a dedicated assumptions tab.

Do I need advanced math skills to build a financial model?

Financial modeling mastery depends more on understanding how financial statements link together than on advanced mathematics. Analysts who grasp the logic of statement linkages consistently build more reliable models than those focused on formula complexity.