A financial contingency plan is a pre-designed response framework that prepares your business to survive and recover from unexpected financial disruptions. Known formally as a contingency capital control system, this type of plan goes well beyond defensive budgeting. Contingency planning is a proactive, pre-engineered system that governs preauthorized actions triggered by measurable financial thresholds. Business owners who create financial contingency plans before a crisis hits preserve negotiation leverage, protect cash flow, and avoid the panic-driven decisions that sink otherwise healthy companies. The steps below give you a clear, practical path to build one.

What does it take to create a financial contingency plan?

Every effective contingency plan starts with three foundational prerequisites: a risk identification audit, a business impact analysis, and a current financial position review. Skip any one of these and your plan will be built on assumptions instead of facts.

Risk identification means listing every scenario that could disrupt your revenue or increase your costs. Think supply chain failures, key client losses, sudden regulatory changes, or a sharp drop in market demand. Rank each scenario by likelihood and potential financial impact so you know where to focus first.

Business impact analysis translates each risk into a dollar figure. How many weeks of revenue would you lose if your top client walked? What would a two-week operational shutdown cost in fixed expenses alone? These numbers become the foundation for your reserve targets.

Financial position review gives you an honest baseline. Pull your current cash balance, outstanding receivables, fixed monthly obligations, and available credit lines. This snapshot tells you how exposed you actually are right now.

Cash categorization and reserve tools

Vanguard's cash strategy recommends categorizing business cash by purpose and timeframe: "today" money covers expenses within 12 months, "someday" money handles unpredictable needs, and "later" money funds long-term goals. This framework prevents you from accidentally tying up contingency funds in illiquid investments when you need them most.

| Prerequisite | Description | Tool |

|---|---|---|

| Risk identification | List and rank financial risk scenarios by likelihood and impact | Risk register template |

| Business impact analysis | Quantify revenue and cost impact of each risk scenario | Scenario planning spreadsheet |

| Financial position review | Snapshot of cash, receivables, fixed costs, and credit lines | Balance sheet, cash flow statement |

| Cash categorization | Allocate reserves by purpose: today, someday, later | Budgeting software |

| Reserve target setting | Set layered milestones starting at $500–$1,000 | Liquidity ratio calculator |

Pro Tip: Start your reserve target small. Financial experts recommend a starter buffer of $500–$1,000 before building toward a full operating reserve. Reaching a small milestone early builds the habit and the confidence to keep going.

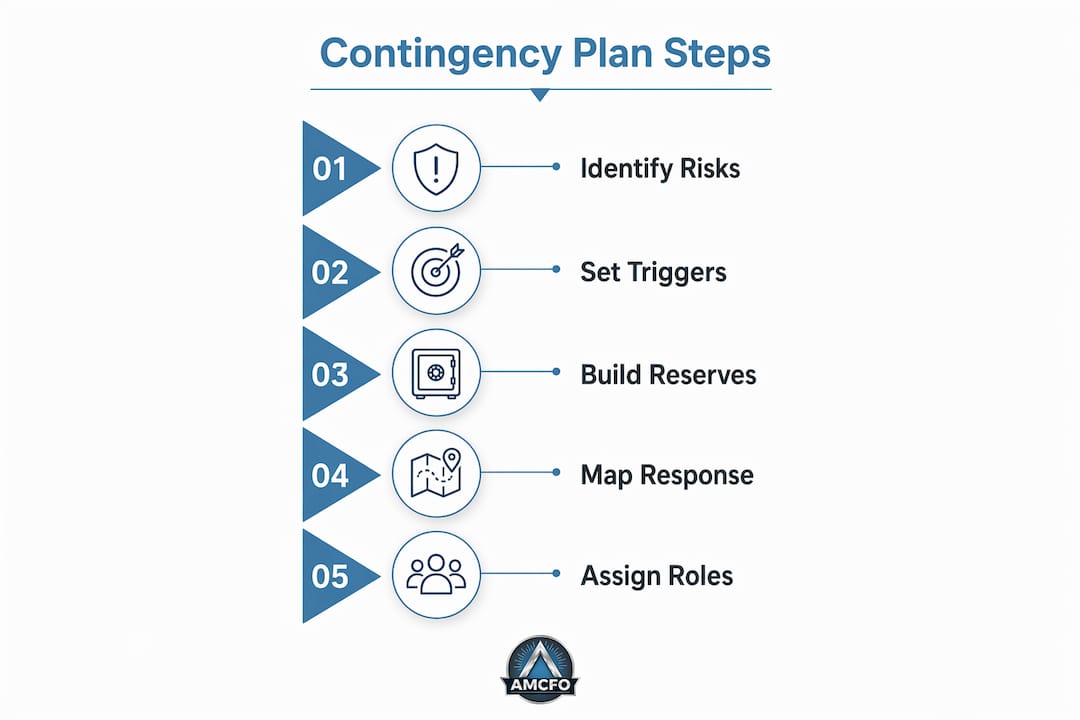

How do you build a financial contingency plan step by step?

The step-by-step process below follows the sequence that financial crisis experts recommend: identify risks, set triggers, build reserves in layers, and define your response sequence before any crisis arrives.

Step 1: Identify and prioritize financial risk scenarios

List every realistic threat to your business finances. Group them into categories: revenue disruption, cost spikes, credit access loss, and regulatory exposure. Prioritize by multiplying likelihood by impact to get a risk score for each scenario.

Step 2: Define measurable trigger points

A trigger is a specific, quantifiable metric that mandates a predefined action the moment it is breached. Examples include: cash runway falling below 60 days, accounts receivable aging past 90 days on more than 20% of your book, or gross margin dropping below a set threshold. Predefined triggers remove subjective judgment from crisis decisions. That removal is the entire point.

Step 3: Build your emergency reserves in layers

Financial experts recommend a three-stage approach to building reserves:

- Starter buffer: $500–$1,000 in a dedicated, liquid account. This covers minor cash gaps without touching operating funds.

- Spending-shock fund: Approximately $2,000 or 0.5 months of operating expenses. This handles sudden, unexpected cost spikes.

- Full operating reserve: 3–6 months of essential operating expenses. The right reserve size depends on your income stability, fixed cost base, and industry risk profile.

Each layer has a different purpose. Do not treat them as one combined pool.

Step 4: Map your crisis response sequence

Poor crisis management almost always follows the same pattern: businesses exhaust cash or cut critical capabilities too early, destroying the value they were trying to protect. The correct crisis response sequence follows this order:

- Internal liquidity optimization (collect receivables faster, delay non-critical payables)

- Cost and capital expenditure deferral (pause discretionary spending)

- Working capital tightening (renegotiate supplier terms, reduce inventory)

- Asset rationalization (sell or lease underused assets)

- Lender engagement and covenant reset (communicate proactively before default)

- External capital injection (raise equity or take on new debt as a last resort)

Following this sequence preserves your negotiation leverage at every stage. Jumping straight to external capital signals desperation and costs you more.

Step 5: Assign roles and document escalation procedures

Every trigger action needs an owner. Assign a named individual to each response step and define who has authority to escalate. Document the entire plan in writing and store it where key personnel can access it immediately. Verbal agreements do not survive a crisis.

Pro Tip: Automate your monitoring where possible. Set up cash flow alerts in your accounting software so you receive a notification the moment a trigger metric approaches its threshold. Early warning beats reactive scrambling every time.

What mistakes should you avoid when implementing a contingency plan?

The most common mistake business owners make is falling into what financial advisors call the "Invincibility Trap." This is the belief that an open line of credit or a high-limit credit card serves as a reliable financial backup plan. Credit access can vanish during economic downturns precisely when you need it most. Banks tighten lending standards in recessions, and credit lines get reduced or revoked without warning.

Other critical mistakes include:

- Tying up contingency capital in illiquid assets. A reserve invested in real estate or long-term securities cannot be accessed in 48 hours. Keep contingency funds in high-yield savings accounts or short-term money market instruments.

- Improvising without predefined protocols. Without a written escalation sequence, decisions get made emotionally under pressure. The result is usually premature cost-cutting that damages the business's core capabilities.

- Failing to update the plan. Regular review and updating of your contingency plan is not optional. Business conditions change, and a plan built on last year's cost structure may be dangerously outdated.

- Skipping contribution discipline. Treat contingency fund contributions like a fixed expense. Automate transfers on a set schedule so the fund grows regardless of monthly cash flow fluctuations.

"A financial contingency plan only works if it is specific enough to execute under pressure. Vague intentions are not a plan."

Pro Tip: Review your contingency plan triggers every quarter. If your business has grown, your trigger thresholds need to grow with it. A 60-day cash runway trigger for a $500,000 revenue business is very different from the same trigger at $5 million.

How do you integrate a contingency plan into your overall business strategy?

A contingency plan that lives in a drawer is not a plan. It is a document. Integration means your financial forecasting process includes contingency scenarios as standard inputs, not afterthoughts.

Practical integration steps include:

- Embed contingency scenarios in your annual budget. Model a base case, an upside case, and a downside case. The downside case is your contingency scenario. Assign probability weights to each.

- Link your plan to your business continuity plan (BCP). A BCP covers operational continuity. Your financial contingency plan covers the capital side. The two must reference each other and share trigger definitions.

- Train key personnel. Every manager who might need to execute a response step should know the plan before a crisis occurs. Run a tabletop exercise once a year where you walk through a simulated trigger event.

- Monitor financial KPIs weekly. Track cash runway, accounts receivable aging, gross margin, and debt service coverage ratio on a consistent schedule. These are your early warning system.

- Coordinate with your lenders and insurers. Share your contingency plan framework with your bank relationship manager. Lenders respond better to borrowers who demonstrate proactive risk management. Review your business interruption insurance annually to confirm coverage aligns with your identified risk scenarios.

Connecting your contingency plan to business financial planning practices at the management level turns a static document into a living operational tool.

Key takeaways

A financial contingency plan works only when it combines predefined triggers, layered reserves, and a sequenced crisis response before any disruption occurs.

| Point | Details |

|---|---|

| Start with prerequisites | Complete a risk audit, business impact analysis, and financial position review before writing your plan. |

| Build reserves in layers | Progress from a $500–$1,000 starter buffer to a full 3–6 month operating reserve in deliberate stages. |

| Define triggers first | Set specific, quantifiable thresholds that mandate action automatically, removing emotion from crisis decisions. |

| Follow the response sequence | Optimize internal liquidity before cutting costs, and engage lenders before seeking external capital. |

| Review and update quarterly | A contingency plan tied to outdated financials provides false confidence, not real protection. |

Why pre-engineered plans outperform reactive ones

Business owners consistently underestimate how fast a financial crisis compresses decision-making time. I have seen companies with strong fundamentals make catastrophic choices in the first 72 hours of a cash crisis, simply because no one had agreed in advance on what to do. The pressure of the moment distorts judgment. Predefined triggers and a written response sequence remove that distortion entirely.

The habit formation piece matters just as much as the plan itself. Nearly half of business owners delay starting contingency planning, which means they are always building reserves reactively, after a scare rather than before one. Starting with a $500 buffer feels almost embarrassingly small. But the discipline of making that first automated transfer, and then the next, is what builds the muscle memory that eventually produces a six-month reserve.

The strategic benefit that most business owners miss is negotiation leverage. A company with three months of cash on hand negotiates with suppliers, lenders, and even clients from a position of strength. A company scrambling for liquidity negotiates from desperation. The difference in outcomes is not marginal. It is often the difference between surviving a downturn and not.

— Angelica

How Amcfo supports your contingency planning

Building a financial contingency plan requires accurate, current financial data as its foundation. Without clean books and reliable cash flow visibility, your trigger thresholds are guesses.

Amcfo's fractional CFO services give business owners and financial managers the expert support needed to design, document, and maintain a contingency plan grounded in real numbers. From accounting and bookkeeping that keeps your financial position current, to scenario modeling and risk assessment, Amcfo brings CFO-level thinking to businesses of every size. If you want a contingency plan that actually works when it matters, the right financial infrastructure makes all the difference.

FAQ

What is a financial contingency plan?

A financial contingency plan is a pre-designed framework of triggers and preauthorized responses that guides a business through unexpected financial disruptions. It differs from a general budget by specifying exact actions tied to measurable financial thresholds.

How much should a business keep in its emergency reserve?

Financial experts recommend building toward 3–6 months of essential operating expenses, starting with a starter buffer of $500–$1,000 and a spending-shock fund of approximately $2,000. The right target depends on your income stability and fixed cost base.

How often should a contingency plan be reviewed?

A contingency plan should be reviewed at least quarterly and updated whenever significant changes occur in business size, cost structure, or risk exposure. Regular review keeps trigger thresholds accurate and response steps executable.

Can a line of credit replace a dedicated contingency fund?

A line of credit is not a reliable substitute for a dedicated reserve. Credit access can be reduced or revoked during economic downturns, exactly when businesses need it most, making a liquid cash reserve the only dependable fallback.

How does a contingency plan connect to a business continuity plan?

A business continuity plan covers operational continuity during disruptions, while a financial contingency plan covers the capital response. The two plans should share trigger definitions and reference each other to create a unified crisis response framework.