Accounts receivable is defined as money owed to a business for goods or services delivered on credit but not yet paid for. It sits on the balance sheet as a current asset, typically collected within a 30–90 day window. That classification matters because it directly affects your liquidity, your ability to pay vendors, and how lenders assess your financial health. Tools like QuickBooks, HighRadius, and AI-driven platforms such as DocSpire have made managing this asset faster and more accurate than ever. Understanding the full receivables lifecycle is the first step toward getting paid on time, every time.

What is the accounts receivable process from start to finish?

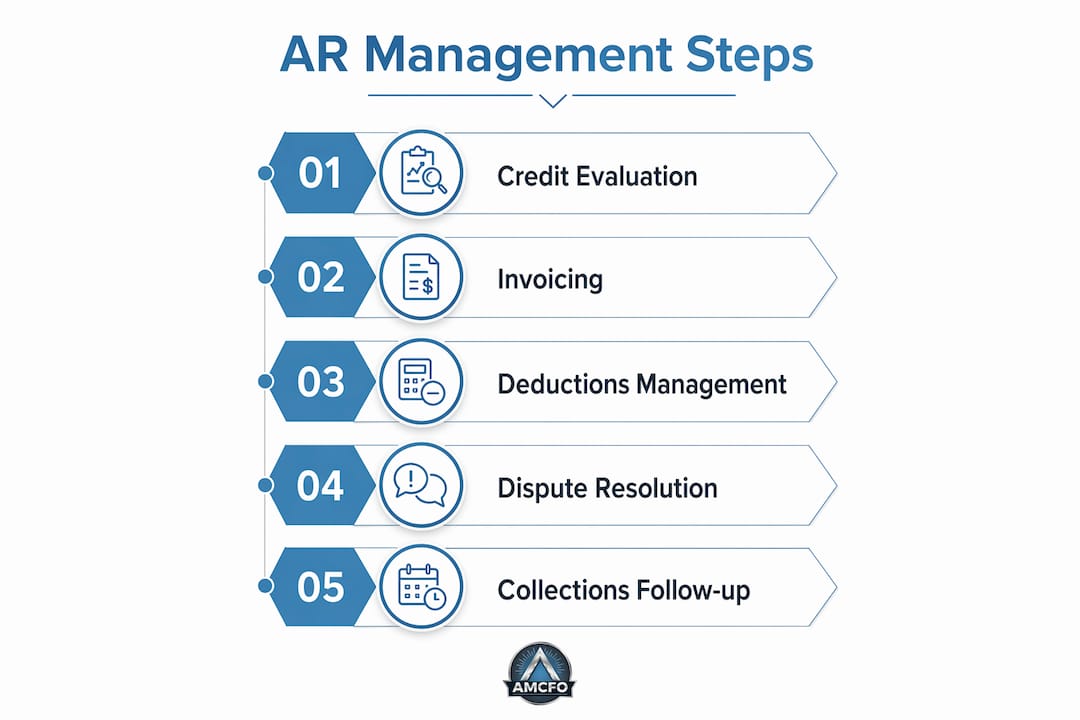

Accounts receivable management is not simply chasing unpaid invoices. It is the full order-to-cash lifecycle that runs from the moment you extend credit to a customer through the moment cash lands in your account.

HighRadius defines this lifecycle around four core pillars:

- Credit evaluation: Assess a customer's creditworthiness before extending payment terms. This is the most important defense against bad debt, yet it is the step most financial managers skip when they are focused only on collections.

- Invoicing: Send accurate, complete invoices immediately after delivery. Errors or delays at this stage push your collection date back by days or weeks.

- Collections management: Run a consistent dunning sequence, escalating reminders from friendly nudges to formal notices. Review aging reports to catch overdue accounts before they become write-offs.

- Cash application and reconciliation: Match incoming payments to the correct invoices quickly. Unmatched payments create false overdue flags and distort your financial reporting.

A fifth element ties these together: dispute resolution. When a customer contests a charge, a clear deductions management process prevents the dispute from stalling payment on the rest of their balance.

Pro Tip: Credit evaluation before extending terms is the single most overlooked step in the receivables process. Skipping it is the fastest route to bad debt.

How can technology and automation transform AR management?

Automation has moved from a nice-to-have to a competitive necessity in accounts receivable. AI-driven invoice tools now achieve up to 99.5% data extraction accuracy and touchless processing rates of 90–94%. That means the vast majority of invoices move through your system without a human touching them.

The practical gains are significant:

- Faster cash application. Automated matching eliminates the manual work of reconciling hundreds of payments against open invoices.

- Fewer errors. Manual data entry introduces mistakes that delay payment and damage customer trust. AI removes that variable.

- Earlier dispute detection. Automated systems flag mismatches in real time rather than waiting for a monthly reconciliation cycle.

- Scalability without headcount. Your AR volume can grow without a proportional increase in staff.

The shift from passive spreadsheets to visual pipeline tracking is equally important. A Kanban-style board that shows every invoice by stage, from sent to overdue to disputed, gives your team immediate visibility. Invoices stop slipping through the cracks because the system makes the gap obvious.

"AR management is not merely collecting owed money but maintaining liquidity by orchestrating the full order-to-cash lifecycle." — HighRadius

Pro Tip: Switch from weekly to daily aging report reviews. A reporting lag of 3–7 days from weekly cycles creates collection backlogs that compound quickly. Daily visibility changes collection behavior at the team level.

Scaling your financial operations with AI-driven workflows is covered in depth in Amcfo's guide on scaling financial operations for growth-stage businesses.

What best practices drive effective AR management?

The most effective accounts receivable strategies combine clear internal policies with consistent customer communication. Technology alone does not close the gap. Stripe's research confirms that business strategy is the critical variable, not the tech stack.

Establish billing and credit policies in writing. Every customer should receive the same payment terms, late fee schedule, and escalation process. Inconsistency invites disputes and signals that your policies are negotiable.

Offer flexible payment options. Customers who can pay by ACH, credit card, or digital wallet pay faster than those limited to paper checks. Reducing friction at the payment step directly shortens your collection cycle.

Track Days Sales Outstanding (DSO) and AR turnover. DSO measures the average number of days it takes to collect after a sale. A rising DSO signals a collections problem before it becomes a cash crisis. AR turnover measures how many times per year you collect your average receivable balance. Both metrics belong in your monthly financial review.

Mature AR software from platforms like HighRadius demonstrates what consistent tracking produces. HighRadius customers report a 10% reduction in DSO and a 40% increase in collection team productivity. Those are not marginal gains. A 10% DSO reduction on $500,000 in annual receivables frees up meaningful working capital.

| Practice | Impact |

|---|---|

| Daily aging report review | Reduces overdue accounts by catching delays early |

| Standardized dunning sequence | Removes guesswork and keeps escalation consistent |

| Flexible payment methods | Shortens collection cycle by reducing payment friction |

| DSO tracking | Gives early warning of collection deterioration |

| Credit evaluation at onboarding | Prevents bad debt before it enters the pipeline |

Pro Tip: Tie your dunning sequence to invoice age, not calendar dates. An invoice 15 days overdue needs a different message than one 45 days overdue. Segment your outreach accordingly.

Good AR practices also connect directly to cash flow management at the business level. The two disciplines reinforce each other.

What financing options complement your receivables strategy?

When collections slow down, receivables financing gives you access to cash without waiting for customers to pay. Two primary options exist: factoring and invoice discounting.

Factoring means selling your outstanding invoices to a third party (a factor) at a discount. The factor collects directly from your customers. You get immediate cash, typically 70–90% of the invoice value upfront, and the factor takes the collection risk. The tradeoff is cost and customer relationship control. Your customers now deal with a third party, which can affect how they perceive your business.

Invoice discounting lets you borrow against your receivables while retaining control of collections. Your customers never know a lender is involved. You pay interest on the amount borrowed and repay it when customers pay you. This option costs less than factoring and preserves the customer relationship, but it requires a stronger internal collections process to manage.

| Option | Best for | Key tradeoff |

|---|---|---|

| Factoring | Businesses with weak collections capacity | Higher cost, loss of customer contact |

| Invoice discounting | Businesses with strong AR processes | Requires disciplined internal collections |

| AR line of credit | Businesses with predictable receivables | Tied to creditworthiness of borrower |

Beyond financing, external debt collection agencies are a last resort for accounts that have aged past 90 days with no response. Agencies typically work on contingency, taking 25–50% of what they recover. The math only works when internal efforts have clearly failed. Before escalating, send a formal demand letter on company letterhead. A significant portion of long-overdue accounts pay after receiving a written demand, without the cost of an agency.

The right financing strategy depends on your industry, customer base, and internal capacity. Integrating a financing option into your AR workflow before you need it, rather than scrambling during a cash crunch, gives you far more negotiating power with lenders and factors.

Key Takeaways

Effective accounts receivable management requires combining clear credit policies, consistent collections processes, and technology to protect cash flow and reduce bad debt.

| Point | Details |

|---|---|

| AR is a current asset | Receivables are reported at net realizable value, not gross invoiced amounts. |

| Automate early and often | AI tools reach 99.5% accuracy and 90–94% touchless rates, cutting manual work significantly. |

| Track DSO monthly | A rising DSO signals a collections problem before it becomes a cash crisis. |

| Credit evaluation comes first | Assessing creditworthiness before extending terms is the most effective bad debt prevention. |

| Financing is a tool, not a fix | Factoring and invoice discounting bridge cash gaps but require a strong underlying AR process. |

Why most AR problems start before the first invoice goes out

After working with businesses across industries, the pattern is consistent. Companies that struggle with collections almost always have the same root problem: they extended credit without a policy. No written terms, no credit check, no escalation process. Then they wonder why customers treat payment as optional.

The fix is not a better dunning email. The fix is treating credit extension as a formal decision, the same way a bank treats a loan application. When you set terms in writing at the start of a customer relationship, you create a reference point for every conversation that follows. The customer signed off on net 30. The invoice says net 30. The reminder references net 30. There is no ambiguity.

Technology matters, but it amplifies whatever process you already have. If your process is inconsistent, automation makes it consistently inconsistent. I have seen businesses invest in AR software and still carry 60-day average DSOs because the underlying credit and collections discipline was never established.

The businesses that collect fastest are not necessarily the ones with the most sophisticated tools. They are the ones with the clearest policies, the most consistent follow-through, and the willingness to have direct conversations with customers when payment is late. Balancing that directness with relationship preservation is the real skill in AR management. It requires judgment, not just software.

— Angelica

How Amcfo helps businesses take control of their receivables

Managing receivables well requires more than a good invoicing tool. It requires accurate books, clear financial reporting, and someone who understands how AR fits into your broader cash position.

Amcfo provides accounting and bookkeeping services built around exactly that. From QuickBooks setup and cleanup to monthly financial reporting, Amcfo keeps your receivables visible and your books accurate. For businesses that need strategic guidance, Amcfo's fractional CFO services bring senior-level financial leadership without the full-time cost. That means help setting credit policies, interpreting DSO trends, and building a collections process that actually works. Contact Amcfo to discuss what your AR process needs to perform at its best.

FAQ

What is accounts receivable in simple terms?

Accounts receivable is money customers owe your business for goods or services already delivered. It is recorded as a current asset on your balance sheet until the customer pays.

How is AR reported on the balance sheet?

AR is reported at net realizable value, meaning the gross amount owed minus an allowance for estimated bad debts. This reflects the cash you actually expect to collect, not the total invoiced amount.

What is a good DSO for a small business?

DSO varies by industry, but a DSO below your standard payment terms (for example, under 30 days on net 30 terms) indicates healthy collections. A rising DSO over consecutive months signals a collections problem that needs immediate attention.

When should I use invoice factoring?

Invoice factoring makes sense when you need immediate cash and your internal collections process cannot close the gap fast enough. The cost is high, so exhaust internal collection efforts and invoice discounting options first.

How often should I review my aging report?

Daily aging report reviews outperform weekly reviews by eliminating the 3–7 day action lag that allows overdue accounts to compound. Daily visibility is the single fastest operational change you can make to improve collections.