Bookkeeping is defined as the systematic recording of every financial transaction a business makes, including sales, expenses, payments, and deposits, forming the foundation for accounting, tax reporting, and every major financial decision you will make as a business owner. Without accurate books, you are flying blind on cash flow, profit margins, and tax obligations. Understanding how bookkeeping works for business is not optional knowledge for small business owners. It is the difference between a company that scales with confidence and one that scrambles every April. Tools like QuickBooks have made the process more accessible, but the underlying logic of recording, categorizing, and reconciling transactions remains the same whether you are a solo freelancer or a 50-person operation.

How bookkeeping works for business: the core workflow

Bookkeeping follows three distinct layers: daily transaction capture, weekly categorization and matching, and monthly close with reconciliation. Each layer builds on the one before it. Skip a layer and errors compound fast.

Here is what each layer looks like in practice:

-

Daily transaction capture. Every sale, expense, vendor payment, and bank deposit gets recorded the day it happens. This prevents the backlog that turns a 20-minute task into a two-day nightmare. Most small business owners spend 15 to 30 minutes daily on this step, which is a realistic and manageable commitment.

-

Weekly categorization and matching. Raw transactions get sorted into categories like payroll, rent, cost of goods sold, and marketing. Bank feeds in QuickBooks or Xero pull transactions automatically, and consistent categorization reduces manual errors significantly. This step typically takes one to two hours per week.

-

Monthly reconciliation and close. You compare your recorded transactions against bank and credit card statements to confirm every dollar is accounted for. After reconciliation, you lock the books. Locking the books prevents retroactive changes that could distort financial reviews or audits. Budget two to three hours monthly for this step, including generating your profit and loss statement and balance sheet.

Pro Tip: Set a recurring calendar block every Friday afternoon for your weekly categorization. Treating it like a meeting you cannot cancel is the single habit that separates business owners with clean books from those who dread tax season.

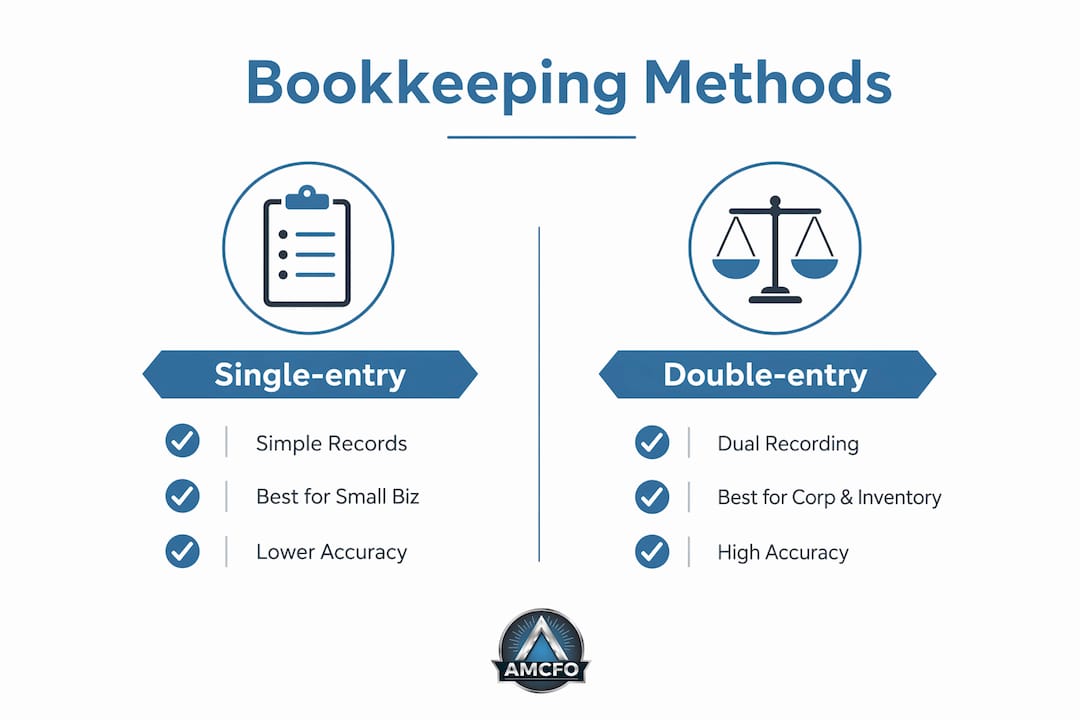

Single-entry vs. double-entry: which method fits your business?

The two foundational methods of business bookkeeping differ in complexity, accuracy, and the type of business each serves best.

| Method | How it works | Best for | Accuracy level |

|---|---|---|---|

| Single-entry | Records each transaction once, like a checkbook register | Sole proprietors, freelancers, very simple businesses | Basic |

| Double-entry | Records each transaction twice as a debit and a credit | LLCs, S-corps, growing businesses, any business with inventory | High |

Double-entry bookkeeping records each transaction twice, with one entry as a debit and one as a credit. When you pay a vendor $500, your cash account decreases by $500 (credit) and your expense account increases by $500 (debit). The two sides always balance, which is exactly how errors get caught before they become tax problems.

Single-entry works like a personal checkbook. You record money in and money out. It is simple, but it gives you no mechanism to detect errors, no balance sheet, and no clear picture of what you owe versus what you own. A freelance graphic designer billing a handful of clients each month can manage with single-entry. A restaurant with inventory, payroll, and vendor accounts cannot.

The practical reality is that most accounting software, including QuickBooks, FreshBooks, and Wave, automates double-entry behind the scenes. You enter a transaction once and the software handles both sides of the entry. This removes the technical barrier that once made double-entry intimidating for small business owners.

Pro Tip: If you are incorporated or carry inventory, start with double-entry from day one. Switching methods mid-year creates reconciliation headaches and can complicate your tax return.

Cash basis vs. accrual basis: how timing changes everything

The accounting method you choose determines when transactions appear in your books, and that timing has real consequences for your tax bill and your understanding of business performance.

Cash basis accounting records revenue and expenses when cash actually changes hands. You invoice a client in December but receive payment in January. Under cash basis, that revenue appears in January. Under accrual basis, it appears in December when the work was completed and the invoice was issued.

Here is a concrete example. A landscaping company completes $8,000 worth of jobs in December but collects payment in January. Under cash basis, December looks like a slow month. Under accrual, December reflects the actual work performed and revenue earned. The difference matters enormously for understanding whether your business is actually growing.

| Scenario | Cash basis result | Accrual basis result |

|---|---|---|

| Invoice sent Dec 15, paid Jan 10 | Revenue recorded in January | Revenue recorded in December |

| Rent paid Jan 1 for December | Expense in January | Expense in December |

| Payroll accrued but not yet paid | Not recorded until paid | Recorded when earned by employees |

Accrual accounting requires managing accounts receivable, accounts payable, deferred revenue, and adjusting entries at month-end. This increases bookkeeping complexity but produces financial statements that reflect economic reality rather than just cash movement. For a growing business seeking a bank loan or outside investment, accrual-basis financials are far more credible and decision-useful.

Cash basis suits service businesses with simple operations, no inventory, and annual revenues under $5 million. Accrual basis suits product businesses, businesses with significant receivables or payables, and any company planning to raise capital or sell. The IRS allows either method for most small businesses, but accrual accounting can appear volatile due to timing differences. Consistency matters most. Switching methods mid-year requires IRS approval and creates comparative reporting problems.

Pro Tip: Not sure which method to choose? Read Amcfo's breakdown of choosing the right accounting method before you set up your books. Getting this decision right at the start saves significant rework later.

How bookkeeping supports tax compliance and financial decisions

Clean books are not just an organizational preference. They are a legal requirement and a strategic asset.

The IRS requires businesses to keep records that substantiate every amount reported on a tax return, covering transactions, assets, payroll, and expenses. Paper or digital formats are both acceptable, but the records must exist and be retrievable. A business that cannot produce receipts during an audit faces disallowed deductions, penalties, and interest charges.

Here is what accurate monthly bookkeeping produces that directly supports your tax and business decisions:

- Profit and loss statement (P&L). Shows revenue, cost of goods sold, and operating expenses for any period. Your CPA uses this to prepare your tax return and you use it to spot where margins are shrinking.

- Balance sheet. Captures what you own (assets), what you owe (liabilities), and your equity at a specific point in time. Lenders require this document before approving any business loan.

- Cash flow statement. Tracks actual cash movement in and out of the business. Profitable companies can still run out of cash, and this report shows you why. Amcfo's guide on cash flow management explains how to use this report to prevent shortfalls.

- Accounts receivable aging report. Lists unpaid invoices by how long they have been outstanding. This report alone can recover thousands in overlooked revenue.

Bookkeeping is the recording layer while accounting handles interpretation, tax returns, and advisory work. The gap between the two functions is where small businesses most often lose money. When your books are disorganized, your accountant spends billable hours cleaning data instead of providing tax strategy. Clean, current books mean your CPA can focus on minimizing your tax liability rather than reconstructing your year.

Keeping bookkeeping current with daily and weekly steps prevents the accumulation of errors that create expensive fixes at tax time. The best bookkeeping practices for small business are not complicated. They are consistent.

Key takeaways

Bookkeeping works by recording every transaction daily, categorizing it weekly, and reconciling it monthly to produce accurate financial reports that drive tax compliance and business decisions.

| Point | Details |

|---|---|

| Three-layer workflow | Daily capture, weekly categorization, and monthly reconciliation form the complete bookkeeping cycle. |

| Double-entry is the standard | Most businesses benefit from double-entry bookkeeping, which catches errors and produces reliable financial statements. |

| Method timing affects taxes | Cash basis records cash movement; accrual records economic activity. Choose based on your business complexity and growth stage. |

| Clean books reduce tax risk | The IRS requires substantiating records for every deduction, making organized bookkeeping a legal necessity, not just good practice. |

| Bookkeeping feeds accounting | Accurate books allow your CPA or CFO to focus on strategy and tax savings rather than data cleanup. |

What I have learned from years of watching small businesses manage their books

The most expensive bookkeeping mistake I see is not fraud or software failure. It is procrastination. Business owners tell themselves they will catch up on the books next week, and next week becomes next quarter, and suddenly they are paying a bookkeeper double to reconstruct nine months of transactions in a panic before the tax deadline.

The second most expensive mistake is treating bookkeeping and accounting as the same function. They are not. Bookkeeping is data entry; accounting is analysis. When a business owner hands their accountant a shoebox of receipts in March, they are paying CPA rates for bookkeeping work. That is a poor use of money and a missed opportunity for real financial guidance.

What actually works is a simple, non-negotiable weekly routine. Fifteen minutes every day and ninety minutes every Friday. That is it. Businesses that maintain this rhythm never face year-end chaos, always know their cash position, and walk into tax season with confidence rather than dread. The payoff is not just financial accuracy. It is the mental clarity that comes from knowing exactly where your business stands at any given moment.

My honest recommendation: if you are spending more than three hours per month on bookkeeping and still feel uncertain about your numbers, you need either better software, a professional bookkeeper, or both. The cost of getting it right is almost always less than the cost of getting it wrong.

— Angelica

Let Amcfo handle your books so you can run your business

If this guide clarified how bookkeeping works but left you wondering whether your current setup is actually doing the job, that is a signal worth acting on. Disorganized or outdated books cost small businesses real money in missed deductions, poor cash flow visibility, and reactive decision-making.

Amcfo provides professional bookkeeping and accounting services built specifically for small and mid-sized businesses. The team handles everything from QuickBooks setup and cleanup to monthly reconciliation, payroll support, and tax coordination. You get accurate, current financials without the overhead of a full-time hire. Whether you need ongoing monthly bookkeeping or a one-time cleanup before tax season, Amcfo delivers the financial clarity your business decisions require. Reach out to discuss what your books need.

FAQ

What is bookkeeping and why does it matter for small businesses?

Bookkeeping is the systematic recording and organizing of every financial transaction a business makes, including sales, expenses, and payments. It forms the foundation for tax filing, financial reporting, and every major business decision.

What is the difference between single-entry and double-entry bookkeeping?

Single-entry records each transaction once, like a checkbook, while double-entry records each transaction as both a debit and a credit. Double-entry is the standard for most businesses because it catches errors and produces accurate financial statements.

Should my small business use cash basis or accrual accounting?

Cash basis suits simple service businesses with straightforward cash flow, while accrual basis better reflects economic activity for businesses with inventory, receivables, or growth plans. The IRS permits either method for most small businesses, but consistency is required once you choose.

How much time should I spend on monthly bookkeeping?

Most small businesses spend 15 to 30 minutes daily on transaction capture, one to two hours weekly on categorization, and two to three hours monthly on reconciliation and report generation. Staying current prevents the costly year-end scramble.

What records does the IRS require businesses to keep?

The IRS requires businesses to maintain records that substantiate all amounts reported on tax returns, covering transactions, assets, payroll, and expenses in either paper or digital format. Retention periods vary by record type, but most business records should be kept for at least three to seven years.