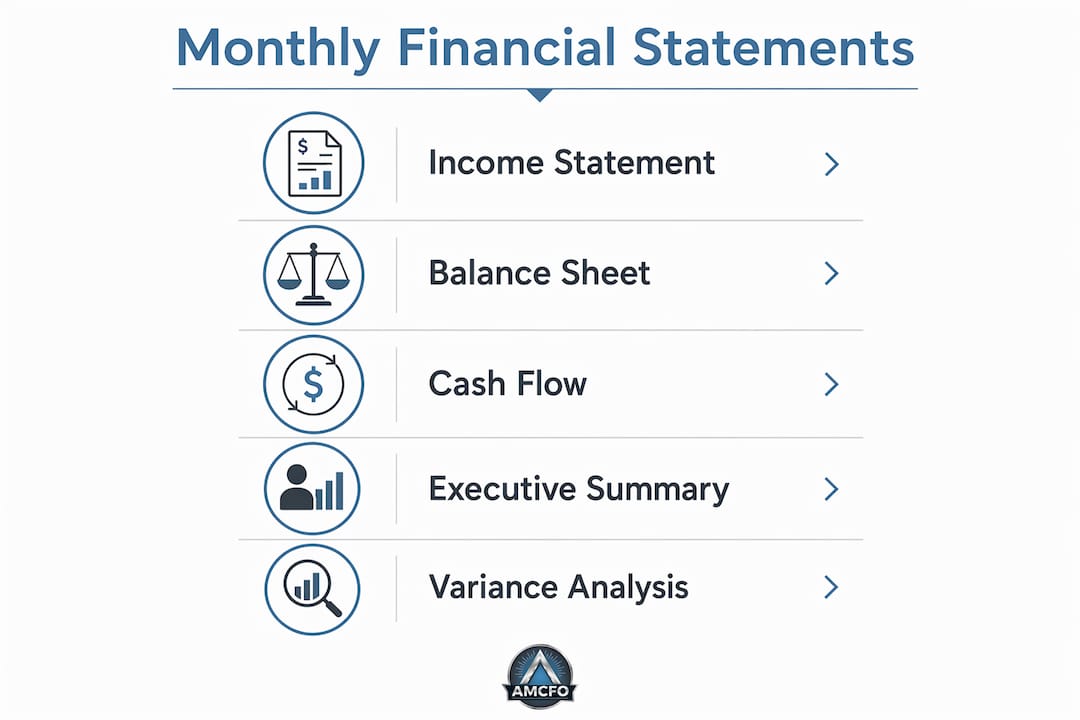

Preparing monthly financial statements is the process of systematically compiling revenue, expenses, assets, and liabilities into three core reports that reflect your business's financial health each month. The three reports are the income statement, the balance sheet, and the cash flow statement. Together, they form the foundation of sound monthly financial reporting and give you the data you need to make confident decisions. Businesses that treat this process as a monthly discipline gain a real advantage: they spot cash problems weeks before they become crises.

How to prepare financial statements monthly: the core reports

The income statement, balance sheet, and cash flow statement must be prepared in that specific order to maintain accuracy and consistency. Each report feeds data into the next, so skipping the sequence creates errors that compound quickly.

The income statement

The income statement summarizes all revenues and expenses for the month and produces a net profit or loss figure. It answers one question: did the business earn more than it spent? A retail business, for example, would list product sales as revenue, then subtract cost of goods sold, payroll, rent, and utilities to arrive at net income. This report is always prepared first because its net income figure flows directly into both the balance sheet and the cash flow statement.

The balance sheet

The balance sheet is a snapshot of your business's financial position at the last day of the month. It lists assets (what you own), liabilities (what you owe), and equity (the difference between the two). A balance sheet that does not balance is a signal of a data entry error or a missing transaction. Reviewing it monthly lets you track whether your debt load is growing relative to your assets.

The cash flow statement

A gap between reported profit and actual cash is common and must be reconciled through the cash flow statement. A business can show a healthy net income on its income statement while running dangerously low on cash because of slow-paying customers or large inventory purchases. The cash flow statement bridges that gap by tracking real cash movements across three categories: operations, investing, and financing. Monitoring it monthly prevents liquidity surprises that can shut down an otherwise profitable business.

A complete monthly financial report also includes an executive summary, key performance indicators, variance analysis, and recommended actions. That structure moves the report from a record-keeping document to a decision-making tool.

What tools and data do you need for monthly statements?

Accurate monthly statements require complete, organized source data. The key records you need before you start are:

- All sales and purchase invoices for the month

- Bank and credit card statements for every account

- Payroll records including wages, taxes, and benefits

- Receipts for any cash expenses

- Loan statements showing interest and principal balances

Timely book closure is critical. Experts recommend closing the books by day 3 after month-end (D+3) and completing bank reconciliations no later than day 5 (D+5). Waiting longer degrades the report's usefulness because decisions get made on stale data.

Accounting method: cash vs. accrual

Your accounting method shapes what your statements show. Cash basis accounting records revenue when cash is received and expenses when cash is paid. Accrual basis accounting records revenue when it is earned and expenses when they are incurred, regardless of when cash moves. Most businesses with inventory or credit sales use accrual accounting because it gives a more accurate picture of profitability. The Generally Accepted Accounting Principles (GAAP) standard requires accrual accounting for most formal financial reporting.

Recommended tools

Accounting software automates many calculations and validations, improving timeliness and accuracy of monthly statements. Cloud-based platforms let multiple team members enter data in real time, which reduces the end-of-month crunch. Spreadsheet templates work for very early-stage businesses but become error-prone as transaction volume grows. A monthly closing checklist is one of the most underused tools: it forces you to confirm every reconciliation step before you finalize the reports.

Pro Tip: Build your closing checklist in a shared document so your bookkeeper and accountant can both check off steps. A missed reconciliation caught at step 4 is far cheaper to fix than one discovered after the reports are distributed.

Step-by-step guide to accurate monthly financial statements

Follow these seven steps every month to produce reliable reports.

- Close the books. Record every transaction that belongs to the month, including accrued expenses and deferred revenue. Do not leave open items to "catch up next month."

- Reconcile all accounts. Match every bank and credit card account to its statement. Misclassified expenses or missing transactions can distort results and mislead decisions, so reconciliation is non-negotiable.

- Prepare the income statement. Pull all revenue and expense accounts for the month. Verify that every expense is coded to the correct category.

- Prepare the balance sheet. Confirm that total assets equal total liabilities plus equity. If they do not, find the discrepancy before moving forward.

- Prepare the cash flow statement. Use the net income from the income statement and the balance sheet changes to calculate actual cash generated or used during the month.

- Run variance analysis. Compare actual results to your budget and to the same month last year. Flag any line item that deviates by more than 10% and write a one-sentence explanation.

- Review, distribute, and act. Check for obvious errors, share the reports with relevant stakeholders, and identify at least one decision the data supports.

Pro Tip: Set a fixed monthly calendar reminder for each closing step. Businesses that treat the close as a project with deadlines finish 40–60% faster than those that approach it informally.

Common mistakes to avoid

The most damaging errors in monthly statement preparation are predictable. Skipping bank reconciliation is the most common. Recording expenses in the wrong period is the second. Mixing personal and business transactions is the third, and it is especially common in sole proprietorships. Each of these errors produces a financial picture that does not reflect reality, which means every decision made from those reports is built on bad data.

Small business owners with accounting knowledge can prepare compiled financial statements internally. Only CPAs may prepare audited or reviewed statements. For most monthly internal reporting, an experienced bookkeeper supported by a fractional CFO covers the full process.

How to interpret monthly statements for cash flow decisions

Reading the numbers is only half the job. The other half is knowing what they mean for your next move.

The most important distinction in monthly reporting is profit versus cash. A business can be profitable and still run out of cash. This happens when customers pay on 60-day terms but suppliers demand payment in 30 days. The cash flow statement reveals this timing mismatch. The income statement does not.

Variance analysis highlights differences between actual results and budget or prior period, driving management decisions. A revenue variance of 15% below budget in march, for example, should trigger an immediate review of the sales pipeline. Waiting until the annual review means three more months of the same shortfall.

Key indicators to track every month include:

- Gross margin: Revenue minus cost of goods sold, expressed as a percentage. A declining gross margin signals pricing pressure or rising input costs.

- Working capital: Current assets minus current liabilities. Negative working capital means the business cannot cover short-term obligations from current resources.

- EBITDA: Earnings before interest, taxes, depreciation, and amortization. It measures operating profitability independent of financing and accounting choices.

- Days sales outstanding (DSO): The average number of days it takes to collect payment after a sale. A rising DSO is an early warning sign of cash flow stress.

Experts recommend tracking 5–8 key indicators focused on the most critical aspects of financial health. More than eight indicators dilutes focus. Fewer than five leaves blind spots.

"Monthly financial reporting transitions a business from reactive bookkeeping to proactive decision-making." The goal is to shrink the time between detecting a financial issue and acting on it.

Customize your monthly report to your business model. A service business should weight DSO and gross margin heavily. A product business should watch inventory turnover and cost of goods sold. A subscription business should track monthly recurring revenue and churn rate. Generic reports answer generic questions. Tailored reports answer the questions that actually drive your business.

For a deeper look at the metrics that matter most, the guide on measuring business financial health covers ratio analysis in practical detail.

Key Takeaways

Preparing monthly financial statements accurately requires completing the income statement, balance sheet, and cash flow statement in sequence, then using variance analysis and key ratios to turn raw numbers into decisions.

| Point | Details |

|---|---|

| Prepare statements in order | Income statement first, then balance sheet, then cash flow statement, to preserve data accuracy. |

| Close books by D+3 | Finalizing records within three days of month-end preserves the reporting value and supports timely decisions. |

| Reconcile every account | Bank and credit card reconciliation catches errors before they distort the final reports. |

| Track 5–8 key indicators | Focus on gross margin, working capital, EBITDA, and DSO to monitor financial health without losing focus. |

| Profit does not equal cash | The cash flow statement reveals liquidity gaps that the income statement hides. |

Monthly reports as a management tool, not a compliance task

Most small businesses I work with treat their monthly financials as something they produce because they have to, not because they want to. That mindset is the single biggest missed opportunity in small business finance.

The businesses that grow consistently are the ones that read their monthly reports the way a pilot reads instruments. They are not looking for confirmation that everything is fine. They are looking for early signals that something needs attention. A gross margin that slips two points in february does not look alarming on its own. But if it slips another two points in march, you have a trend. Catching that trend at month two instead of month six is the difference between a pricing adjustment and a cash crisis.

The other pattern I see constantly is businesses that prepare the reports but never act on them. The variance analysis column stays blank. The cash flow statement gets filed without anyone asking why cash dropped $30,000 in a month when net income was positive. Reports without interpretation are just paper. The value is in the conversation the numbers start.

Technology has made the mechanical side of monthly reporting faster than ever. The constraint now is not data entry. It is the discipline to sit down with the numbers, ask hard questions, and make a decision before the month gets away from you. That discipline is what separates businesses that scale from businesses that survive.

For practical guidance on building financial strategies for growth, the frameworks that work for small businesses are simpler than most owners expect.

— Angelica

Amcfo's accounting and fractional CFO services for monthly reporting

Producing accurate monthly financial statements takes consistent effort, the right tools, and someone who knows what to look for in the numbers.

Amcfo provides accounting and bookkeeping services designed to keep your books current, your accounts reconciled, and your monthly reports ready on time. For businesses that need more than clean books, Amcfo's fractional CFO services add the layer of financial analysis and strategic guidance that turns monthly reports into growth decisions. Whether you need a full monthly close process or a senior financial advisor to interpret the results, Amcfo builds the support around what your business actually needs.

FAQ

What are the three main financial statements prepared monthly?

The three core monthly financial statements are the income statement, the balance sheet, and the cash flow statement. They must be prepared in that order because each report uses data from the previous one.

How long does it take to prepare monthly financial statements?

The timeline depends on business complexity and how current the books are. Closing the books by day 3 after month-end and completing reconciliations by day 5 is the standard recommended by accounting professionals.

Can a small business owner prepare financial statements without a CPA?

Small business owners and employees with accounting knowledge can prepare compiled financial statements internally. Only CPAs may prepare audited or reviewed statements, which are required for external financing or regulatory purposes.

What is the difference between cash basis and accrual accounting for monthly statements?

Cash basis records transactions when cash changes hands. Accrual basis records them when they are earned or incurred. GAAP requires accrual accounting for most formal reporting, and it gives a more accurate monthly picture of profitability.

Why does monthly cash flow differ from monthly profit?

Profit measures revenue minus expenses on an accrual basis. Cash flow tracks actual money moving in and out of the business. Timing differences, such as unpaid invoices or prepaid expenses, create a gap between the two figures that the cash flow statement explains.