Financial reporting is the accounting process businesses use to prepare and share financial data that reflects performance and financial position. Done well, it gives you and your stakeholders a clear, accurate picture of where the company stands. Done poorly, it creates compliance risk, audit failures, and decisions built on faulty numbers. This guide covers the major frameworks, core financial statements, tiered compliance strategies, and the best practices that separate reliable reports from ones that cause problems.

What is financial reporting and why does it matter?

Financial reporting is the structured process of compiling, presenting, and communicating a company's financial information to internal and external stakeholders. The output includes financial statements, disclosures, and supporting notes that together tell the full story of a business's financial health. Investors, lenders, regulators, and your own management team all rely on this information to make decisions.

The process goes beyond data entry. Financial reporting transforms raw transactional accounting data into meaningful information that stakeholders can actually use. Without that translation, it becomes nearly impossible to distinguish operational efficiency from a temporary cash spike.

Two governing bodies shape how most of this works: the Financial Accounting Standards Board (FASB), which oversees U.S. GAAP, and the International Accounting Standards Board (IASB), which governs IFRS. Knowing which one applies to your business is the starting point for every reporting decision you make.

What are the main financial reporting frameworks?

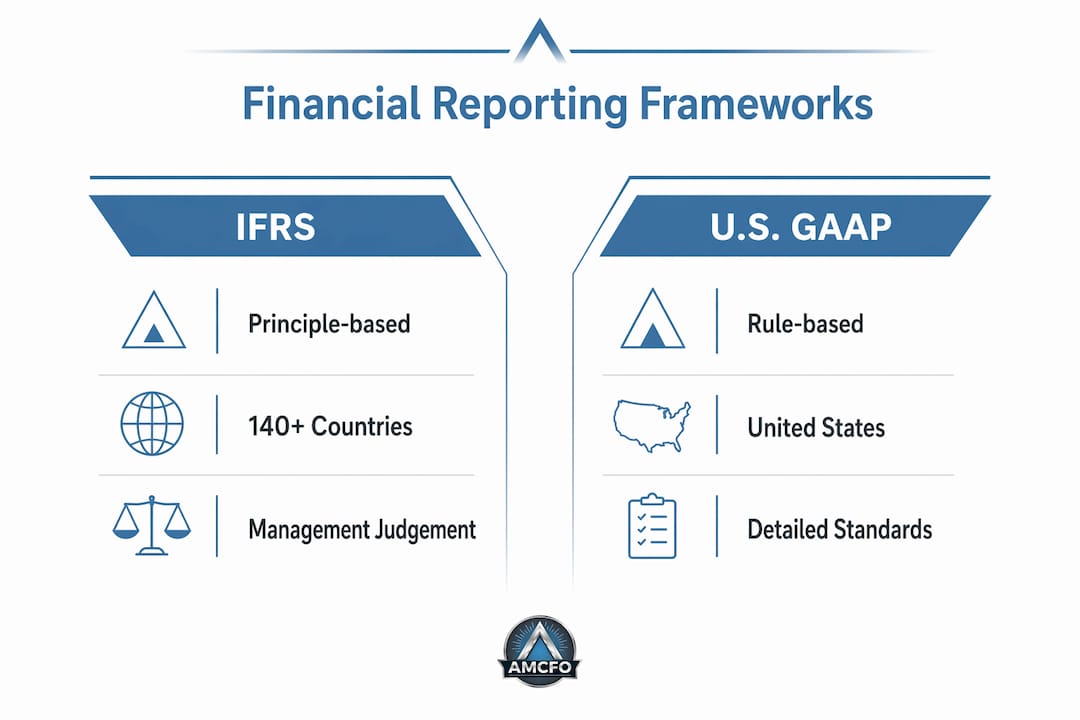

IFRS vs. u.s. GAAP: the core difference

IFRS is a principle-based system used in over 140 countries, including two-thirds of the G20. U.S. GAAP, governed by FASB, is a rule-based system used almost exclusively in the United States. That distinction matters more than it sounds.

A principle-based system gives management more discretion. You apply judgment to recognize revenue, measure leases, and account for income taxes. A rule-based system provides specific guidance for specific situations, which reduces ambiguity but also creates more complexity. The same lease transaction can appear very differently on an IFRS balance sheet versus a GAAP one.

Framework differences affect reported revenues, leases, and income taxes in ways that make direct comparisons between companies difficult. If you are raising capital from international investors or planning a cross-border acquisition, this is not a minor technical detail. It changes the numbers your counterparty sees.

How to choose the right framework

| Factor | IFRS | U.S. GAAP |

|---|---|---|

| Geographic scope | 140+ countries | United States only |

| Approach | Principle-based | Rule-based |

| Flexibility | Higher managerial judgment | Specific rules per transaction |

| Best for | Multinational or global entities | U.S.-based private and public companies |

| Governing body | IASB | FASB |

The choice of framework depends on your entity's legal structure, size, and jurisdiction. A U.S.-based private company with no foreign investors will almost always use GAAP. A company seeking foreign investment or listing on an international exchange needs to consider IFRS.

Pro Tip: If your business is growing toward a capital raise or acquisition, ask your accountant now whether your current framework aligns with what your future investors will expect. Switching frameworks mid-process is expensive and time-consuming.

What financial statements make up a complete report?

A complete set of financial statements includes five core documents. Each one answers a different question about your business.

- Balance sheet: Shows what the company owns (assets), what it owes (liabilities), and what is left for owners (equity) at a specific point in time.

- Income statement: Reports revenues, expenses, and net profit or loss over a period. This is the document most business owners look at first.

- Cash flow statement: Tracks the actual movement of cash through operating, investing, and financing activities. Profit and cash are not the same thing, and this statement shows why.

- Statement of changes in equity: Explains how the ownership stake in the business changed during the period, including retained earnings and any distributions.

- Notes and disclosures: Provide the context behind the numbers. They explain accounting policies, significant judgments, and any items that could affect how you interpret the statements.

These five documents work together. A company can show strong net income on the income statement while running out of cash, which the cash flow statement will reveal. The notes explain whether a spike in revenue reflects real growth or a one-time accounting adjustment.

Report complexity scales with entity size. A small business may produce a simplified income statement and balance sheet. A public company must include full disclosures, segment reporting, and auditor sign-off. The level of detail required is not arbitrary. It reflects the number of stakeholders who depend on the information.

How do tiered frameworks help smes and nonprofits?

Not every business needs the same level of reporting detail. A tiered approach to financial reporting standards adjusts requirements based on entity size and sector. This keeps compliance costs proportional to the actual information needs of your stakeholders.

Excessive disclosure can obscure key business performance rather than clarify it. A 200-page annual report built for a public company creates more confusion than confidence when applied to a 15-person manufacturing firm. Tiered frameworks solve this by matching disclosure depth to audience need.

Here is how the tiers typically work in practice:

- Public companies: Full GAAP or IFRS compliance, including segment reporting, earnings per share, and comprehensive footnote disclosures.

- Private companies: Reduced disclosure requirements under frameworks like the AICPA's Financial Reporting Framework for Small and Medium-Sized Entities (FRF for SMEs), which simplifies lease accounting and goodwill treatment.

- Nonprofits: Follow FASB's ASC 958, which replaces the equity section with net assets and requires specific fund accounting disclosures.

- Micro-entities: May use cash-basis or modified cash-basis reporting, which tracks actual cash in and out rather than accrual-based recognition.

Public entities often require full GAAP compliance, while SMEs benefit from simplified formats with fewer disclosure requirements. That flexibility is not a loophole. It is a deliberate design choice to make compliance achievable without a full-time accounting department.

For SMEs managing cash flow alongside compliance, simplified reporting frameworks reduce the administrative burden without sacrificing the core financial picture lenders and owners need.

Pro Tip: If you are a private company using full GAAP when a simplified framework would satisfy your lenders and investors, you may be spending money on compliance you do not need. Ask your accountant to review whether a tiered option fits your situation.

What are the best practices for accurate financial reporting?

Reliable financial reports do not happen by accident. They require consistent processes, clear policies, and disciplined reconciliation at every stage of the reporting cycle.

-

Maintain a complete audit trail. Every transaction should be traceable from the source document to the final report. Failing to reconcile segment-level data increases audit risk and breaks data comparability across periods. A missing receipt or an unreconciled intercompany transaction can delay an audit by weeks.

-

Apply accounting policies consistently. Switching from cash-basis to accrual accounting mid-year, or changing your revenue recognition method without proper documentation, creates gaps that auditors flag immediately. Consistency is what makes year-over-year comparisons meaningful.

-

Reconcile operational data to your closing package. The quality of financial reporting depends heavily on the integrity of the reconciliation between operational-level data and the closing package. This means your bank statements, accounts receivable aging, and inventory counts must all tie back to what appears in the final report.

-

Separate duties where possible. The person who records transactions should not be the same person who approves them. This is a basic internal control that reduces both error and fraud risk.

-

Review reports before distribution. A financial manager should read every report before it goes to a lender, investor, or board member. Numbers that look unusual often signal a posting error or a classification mistake that is easy to fix before it becomes a problem.

"Maintaining consistency through rigorous reconciliation processes is fundamental to preventing regulatory issues and improving report comparability year-over-year." — GAO Report on Financial Reporting Quality

Following financial reporting best practices consistently is what separates businesses that sail through audits from those that spend months correcting prior-period errors.

Key takeaways

Accurate financial reporting requires the right framework, complete financial statements, and consistent reconciliation processes applied every reporting period.

| Point | Details |

|---|---|

| Framework choice matters | Select IFRS or U.S. GAAP based on your legal structure, size, and investor base. |

| Five statements tell the full story | Balance sheet, income statement, cash flow, equity changes, and notes work together. |

| Tiered compliance saves money | SMEs and nonprofits can use simplified frameworks without sacrificing core transparency. |

| Reconciliation prevents audit failures | Consistent reconciliation between operational data and closing packages is non-negotiable. |

| Consistency builds comparability | Applying the same accounting policies each period makes your reports meaningful over time. |

Why financial reporting is really a translation problem

I have worked with business owners who had perfectly accurate bookkeeping and still could not answer basic questions about their own profitability. The numbers were there. The translation was missing.

Financial reporting is not just a compliance exercise. It is the process of converting raw accounting data into language that decision-makers can actually use. When that translation layer breaks down, you get reports that are technically correct but practically useless. A balance sheet that no one reads is not an asset. It is a liability.

What I have seen consistently is that the businesses with the strongest reporting are not necessarily the ones with the most sophisticated software. They are the ones with clear policies, disciplined month-end processes, and someone who actually reviews the output before it gets filed or distributed. The tool matters less than the process behind it.

The other thing most articles will not tell you: the notes and disclosures section of a financial report is often more valuable than the statements themselves. That is where the judgment calls live. That is where you find out whether revenue recognition is aggressive or conservative, whether a lease obligation is buried or disclosed, and whether management is being straight with you about the risks. If you are reading reports for any business, start with the notes.

High-quality reporting also changes how your stakeholders treat you. Lenders extend better terms to businesses that produce clean, consistent reports. Investors move faster when the numbers are clear. And your own management team makes better decisions when the financial picture is accurate and timely. That is not a soft benefit. It is a direct competitive advantage.

— Angelica

How Amcfo helps you report with confidence

Producing accurate, compliant financial reports takes more than good intentions. It takes the right processes, the right people, and a clear understanding of which standards apply to your business.

Amcfo provides bookkeeping, accounting, and fractional CFO services tailored to businesses at every stage of growth. Whether you need help setting up your chart of accounts, cleaning up prior-period errors, or building a monthly reporting package your lenders will trust, Amcfo has the expertise to get it done. Our accounting and bookkeeping services are built around the specific compliance and reporting needs of your business, not a one-size-fits-all template. If your reports are not giving you the clarity you need to make confident decisions, that is exactly the problem Amcfo is built to solve.

FAQ

What is financial reporting in simple terms?

Financial reporting is the process of preparing and sharing financial statements that show a company's performance and financial position. It communicates key data to investors, lenders, and management.

What is the difference between IFRS and u.s. GAAP?

IFRS is principle-based and used in 140+ countries, while U.S. GAAP is rule-based and applies almost exclusively in the United States. The choice depends on your jurisdiction, legal structure, and investor base.

How often should a business prepare financial reports?

Most businesses prepare monthly internal reports and annual reports for tax and compliance purposes. Lenders and investors may require quarterly reporting depending on your agreements.

What skills does financial reporting require?

Core skills include management, communication, Microsoft Excel, attention to detail, and problem-solving. These competencies support accurate data handling and clear stakeholder communication.

Can small businesses use simplified financial reporting?

Yes. Frameworks like the AICPA's FRF for SMEs and other tiered standards allow smaller businesses to meet compliance requirements with fewer disclosure obligations than public companies face.