Most small business owners use the terms bookkeeping and accounting interchangeably, and that mix-up costs them. Getting bookkeeping vs accounting explained clearly matters because hiring the wrong professional, or skipping one function entirely, creates financial blind spots that compound over time. Bookkeeping and accounting are distinct disciplines that work together. One captures what happens in your business financially; the other tells you what it means. This guide breaks down each role, compares them side by side, and gives you practical guidance on how to manage both without overpaying or underinvesting.

Table of Contents

- Key takeaways

- What bookkeeping actually is

- What accounting actually does

- Bookkeeping vs accounting: a side-by-side comparison

- Practical steps to manage both effectively

- Common mistakes that cost small business owners money

- My take on what actually separates thriving businesses from struggling ones

- Get financial clarity with Amcfo's expert support

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Bookkeeping records transactions | Bookkeepers capture daily financial activity so your records stay current and accurate. |

| Accounting interprets the data | Accountants transform your bookkeeping records into reports that support decisions and compliance. |

| Both roles are necessary | Skipping either function creates gaps in financial visibility that hurt planning and tax work. |

| Clean books reduce accounting costs | Organized bookkeeping data cuts the time accountants spend reconstructing records, lowering your bill. |

| Know when to hire which | Start with a bookkeeper early, then add accounting support as your business grows in complexity. |

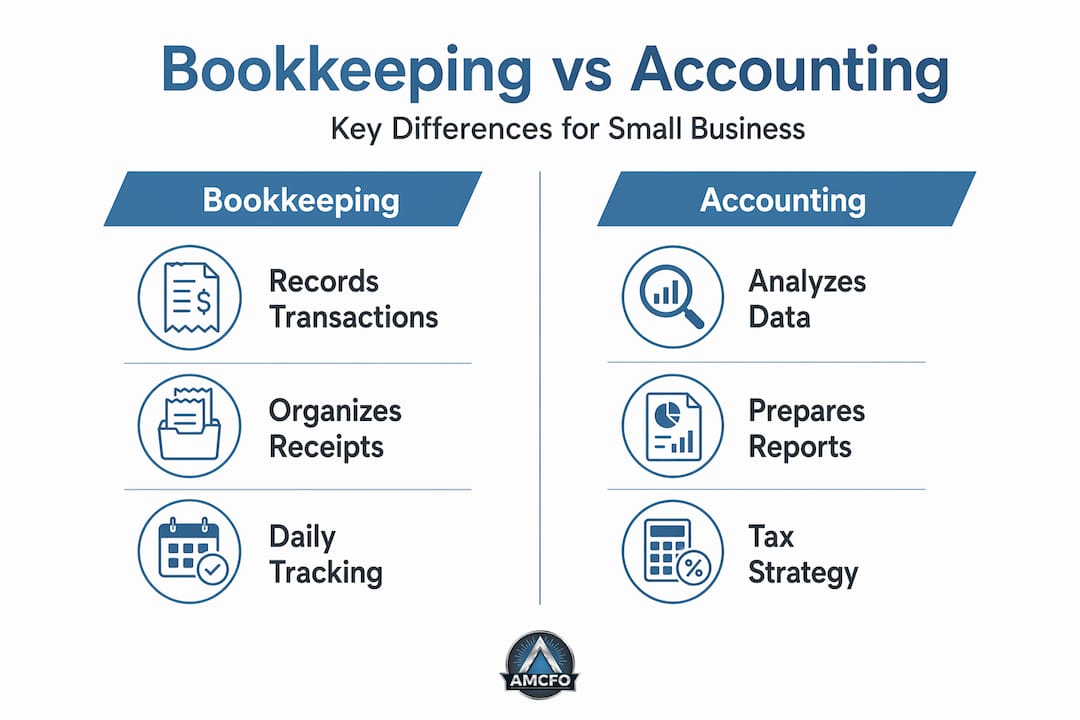

What bookkeeping actually is

Bookkeeping is the day-to-day process of recording, organizing, and storing every financial transaction your business makes. Think of it as the foundation. Without it, accounting has nothing to work with.

A bookkeeper's job centers on keeping your records current and correct. Their typical responsibilities include:

- Recording sales, purchases, and payments as they happen

- Maintaining the general ledger where every transaction is categorized

- Reconciling bank and credit card statements each month

- Tracking accounts receivable (money owed to you) and accounts payable (money you owe)

- Managing payroll records and expense documentation

- Organizing receipts and supporting documents for each transaction

What trips up a lot of small business owners is thinking bookkeeping is just data entry. Bookkeeping also involves document organization and completeness checks that are necessary for accurate accounting down the line. If a receipt is missing or a transaction is categorized incorrectly, that error travels forward into every report your accountant produces.

The software side of bookkeeping has made the work more accessible. Tools like QuickBooks, Xero, and FreshBooks handle much of the mechanical recording, though someone still needs to review the inputs, fix miscategorizations, and run monthly reconciliations. Bookkeepers' core value is organizing and storing records so that accounting and tax preparation runs faster and with fewer surprises.

Pro Tip: Clean, well-categorized books directly reduce what you pay an accountant. When a bookkeeper delivers reconciled, organized records, your accountant spends time analyzing and advising, not reconstructing what happened. That shift alone can cut accounting fees significantly.

What accounting actually does

Accounting picks up where bookkeeping leaves off. While bookkeeping captures the financial story transaction by transaction, accounting converts those details into information used to evaluate your business's financial health and plan for the future.

An accountant's responsibilities go considerably further than maintaining records. Their work typically includes:

- Preparing financial statements: the income statement, balance sheet, and cash flow statement

- Analyzing profitability by product, service line, or time period

- Handling tax preparation, filing, and compliance

- Identifying trends and anomalies in your financial data

- Supporting budgeting and financial forecasting

- Advising on business structure, cost control, and growth strategy

There are two broad categories worth knowing. Financial accounting focuses on external reporting, producing statements that lenders, investors, or tax authorities rely on. Managerial accounting focuses internally, generating reports that help you and your leadership team make decisions. Both use the same underlying data your bookkeeper maintains.

The key distinction is interpretation. A bookkeeper tells you what happened. An accountant tells you what it means and what to do about it. For example, your bookkeeper records that revenue rose 18% last quarter. Your accountant analyzes whether that growth is sustainable, where margin is being lost, and whether cash flow can support expansion. That analysis has direct value for anyone thinking about smarter business decisions.

Bookkeeping vs accounting: a side-by-side comparison

Here is where the differences between bookkeeping and accounting come into sharp focus. The comparison below shows how the two functions differ across the tasks that matter most to you as a business owner.

| Area | Bookkeeping | Accounting |

|---|---|---|

| Primary focus | Recording and organizing transactions | Analyzing and interpreting financial data |

| Typical tasks | Data entry, reconciliations, ledger maintenance | Financial statements, tax prep, forecasting |

| Skills required | Attention to detail, software proficiency | Analytical thinking, regulatory knowledge |

| Certifications | Often none required; some hold CPB credentials | CPA or CMA common; required for certain filings |

| Output | Organized, current financial records | Reports, insights, compliance documents |

| Decision support | Minimal | High |

Bookkeepers manage ongoing recording tasks while accountants handle higher-level analysis, reporting, and tax work. The two roles are designed to work together, not replace each other. Your bookkeeper feeds accurate data to your accountant. Your accountant uses that data to produce reports and guidance you can act on.

From a cost standpoint, bookkeeping is typically less expensive per hour than accounting work. That makes logical sense since the skill requirements differ. Hiring a CPA to do data entry is like paying a surgeon to take your blood pressure. For most small businesses, the right approach is to maintain ongoing bookkeeping and bring in accounting support monthly, quarterly, or around tax season depending on complexity.

Pro Tip: If your accountant regularly spends time fixing categorization errors or tracking down missing transactions, that is a sign you need better bookkeeping support, not more accounting hours. Address the foundation first.

Practical steps to manage both effectively

Understanding the difference between the two functions is one thing. Building a working system is another. Here is how to set up bookkeeping and accounting that actually support your business without unnecessary expense.

Step 1: Get your bookkeeping set up from day one. The earlier you establish consistent recordkeeping, the less cleanup you face later. Choose software that matches your business size and transaction volume. QuickBooks Online works well for most small businesses. Set up your chart of accounts to reflect how your business actually operates.

Step 2: Establish a monthly close routine. A monthly close process involves your bookkeeper producing reconciled ledgers that accountants then transform into financial statements. Build this rhythm early, even if the statements are simple. Monthly visibility beats scrambling at year-end.

Step 3: Separate your business and personal finances completely. This is the most common mistake new business owners make. Mixing accounts creates reconciliation nightmares and complicates tax work dramatically. Open a dedicated business checking account and credit card before you run a single transaction.

Step 4: Hire a bookkeeper before you think you need one. Most business owners wait too long. If you are spending more than three hours per week managing your own books, the cost of a part-time bookkeeper almost certainly makes financial sense.

Step 5: Add accounting support as complexity grows. When you hire employees, take on investors, pursue financing, or face more complex tax situations, bring in a qualified accountant. Their ability to interpret your financials and guide decisions will pay for itself. Consider reviewing how to choose the right accounting method early so you start on the right foundation.

Good financial documentation makes every step easier. Keep digital copies of receipts, invoices, and contracts organized by month. The cleaner your records, the less time any professional spends doing detective work on your behalf.

Common mistakes that cost small business owners money

Even with the best intentions, small business owners regularly fall into patterns that make both bookkeeping and accounting more expensive and less useful.

Here are the most common pitfalls to avoid:

- Treating bookkeeping as optional until tax season. When records pile up for months, accountants or bookkeepers must reconstruct transactions under pressure, which raises costs and increases error risk. Year-round bookkeeping is cheaper than emergency catch-up work.

- Mixing up the roles when hiring. Some business owners hire a bookkeeper and expect accounting-level advice. Others hire an accountant to do bookkeeping-level tasks. Both mismatches waste money and leave gaps in coverage.

- Ignoring the reports accounting produces. Inconsistent bookkeeping records complicate accounting, but ignoring the resulting reports wastes the whole investment. Reading your income statement and cash flow report monthly is non-negotiable if you want to make good decisions.

- Underestimating regulatory requirements. Tax deadlines, payroll filings, and compliance reports are not forgiving. Missing them carries penalties. Accurate, timely bookkeeping feeds into these obligations directly.

- Thinking software replaces professional judgment. QuickBooks can record a transaction. It cannot tell you whether a contract structure is putting your margins at risk. Software supports the work; professionals guide it.

The cost of avoiding professional financial help almost always exceeds the cost of hiring it. What looks like savings tends to show up later as penalties, missed opportunities, or financial surprises that a monthly accounting review would have flagged early.

My take on what actually separates thriving businesses from struggling ones

I have worked with enough small businesses to see a pattern that nobody talks about enough. The ones that grow steadily and weather hard quarters are not necessarily the ones with the best products or the most aggressive marketing. They are the ones that know their numbers.

That starts with bookkeeping. In my experience, business owners who treat bookkeeping as a back-office chore rather than a strategic input are constantly reacting instead of planning. They find out cash is tight when the bank account says so, not when a report warned them three weeks earlier. That lag is expensive.

What I have also seen is a real gap between what bookkeeping delivers and what accounting needs. I have sat with accountants who received books that were technically recorded but not actually organized for reporting. Wrong categories, missing month-end reconciliations, transactions lumped together because nobody wanted to figure out how to split them. That gap costs real money in accounting hours and produces reports you cannot fully trust.

My honest advice: stop thinking of bookkeeping and accounting as expenses and start treating them as inputs to your decision-making. The management accounts you get from a tight bookkeeping and accounting process are the closest thing to a GPS for your business. Without them, you are navigating by feel. With them, you can see where you are, where you are heading, and what levers to pull.

— Angelica

Get financial clarity with Amcfo's expert support

Running a business is demanding enough without untangling the difference between your books and your reports on your own. Amcfo provides professional bookkeeping and accounting services built specifically for small businesses and growing companies that need accurate records and real financial insight, not generic advice.

From QuickBooks setup and monthly reconciliations to financial statement preparation and tax coordination, Amcfo's team handles the full financial workflow so nothing falls through the cracks. And when your business needs more than reports, Amcfo's fractional CFO services give you senior-level financial strategy without the cost of a full-time hire. Whether you need cleaner books, sharper reports, or a financial partner who understands where your business is headed, Amcfo is built for exactly that.

FAQ

What is the main difference between bookkeeping and accounting?

Bookkeeping records daily financial transactions, while accounting analyzes those records to produce reports, support tax compliance, and guide business decisions. Both are necessary, but they serve distinct purposes.

Do small businesses need both a bookkeeper and an accountant?

Most small businesses benefit from both. A bookkeeper keeps records current throughout the year, while an accountant interprets that data for financial statements, tax filings, and strategic planning.

What does a bookkeeper do on a daily basis?

A bookkeeper records transactions, maintains the general ledger, reconciles bank accounts, tracks invoices and bills, and organizes financial documents. Their work keeps your financial data accurate and current.

When should I hire an accountant for my small business?

Bring in an accountant when you need financial statements, tax preparation, compliance support, or guidance on business growth. Accountants add the most value when clean bookkeeping data is already in place.

Can accounting software replace a bookkeeper or accountant?

No. Software records and organizes data, but it cannot interpret what the numbers mean, catch strategic errors, or provide advice. Professional judgment from a bookkeeper and accountant remains necessary for reliable financial management.