Bookkeeping is the systematic process of recording and organizing every financial transaction a business makes, and it is the foundation every sound financial decision rests on. Understanding why bookkeeping matters for business goes beyond keeping the IRS satisfied. Accurate books give you real visibility into cash flow, profitability, and where your money actually goes. Without that visibility, you are making decisions based on guesswork. The Generally Accepted Accounting Principles (GAAP) and IRS recordkeeping requirements both treat organized financial records as non-negotiable, and for good reason.

Why bookkeeping matters for business financial organization

Disorganized finances are one of the fastest ways to lose control of a business. Bookkeeping gives you a clear, current picture of every dollar coming in and going out. That clarity prevents the three most common and costly mistakes small business owners make: missed vendor payments, duplicate expenses, and unexpected cash shortages.

Tracking income and expenses methodically means you always know your working capital position. You can see whether a slow month is a trend or a one-time dip. You can spot a vendor overcharging you before it compounds across twelve invoices.

Relying on your bank balance alone is a dangerous habit. Bank balances can mask declining margins, outstanding liabilities, and cash flow crunches that do not show up until it is too late. A formal income statement, produced through consistent bookkeeping, reveals the true financial health of your business.

Cash flow forecasting also depends entirely on clean books. When your records are current, you can project the next 60 or 90 days with confidence. That kind of foresight lets you time major purchases, negotiate better payment terms, and avoid borrowing at the worst possible moment.

- Record every transaction at the time it occurs, not at month-end

- Categorize expenses correctly from day one to simplify tax prep later

- Reconcile accounts monthly to catch errors before they compound

- Separate business and personal finances with dedicated accounts

- Use consistent chart-of-accounts categories across every period

Pro Tip: Monthly reconciliation is the gold standard for accuracy. Accountants charge premium fees to clean up disorganized year-end records. Doing it monthly costs far less and keeps you audit-ready year-round.

How does bookkeeping protect you from tax problems?

The IRS requires businesses to maintain records that support every item reported on a tax return. Failing to do so exposes you to penalties, interest charges, and the cost of a full audit. Maintaining year-round records saves thousands in accounting fees compared to scrambling through disorganized receipts at year-end.

Accurate bookkeeping does more than keep you compliant. It actively puts money back in your pocket. When expenses are properly categorized throughout the year, you capture every deductible dollar. Timely bookkeeping enables businesses to take full advantage of tax deductions because expenses are easy to find and already categorized correctly.

The consequences of poor recordkeeping compound quickly:

- Missed deductions reduce your net income on paper, meaning you pay more tax than you owe

- Inaccurate filings trigger IRS notices and potential penalties that cost more than the original error

- Audit exposure increases when records are incomplete or inconsistent across periods

- Late filing fees stack on top of any tax owed when disorganized books delay your return

Organized financial records simplify tax preparation and reduce the risk of penalties during audits. That is not just a best practice. It is the difference between a smooth tax season and a stressful, expensive one.

Pro Tip: Keep digital copies of all receipts and match them to your bookkeeping entries monthly. If the IRS ever requests documentation, you want every record one click away, not buried in a shoebox.

Can bookkeeping actually drive business growth?

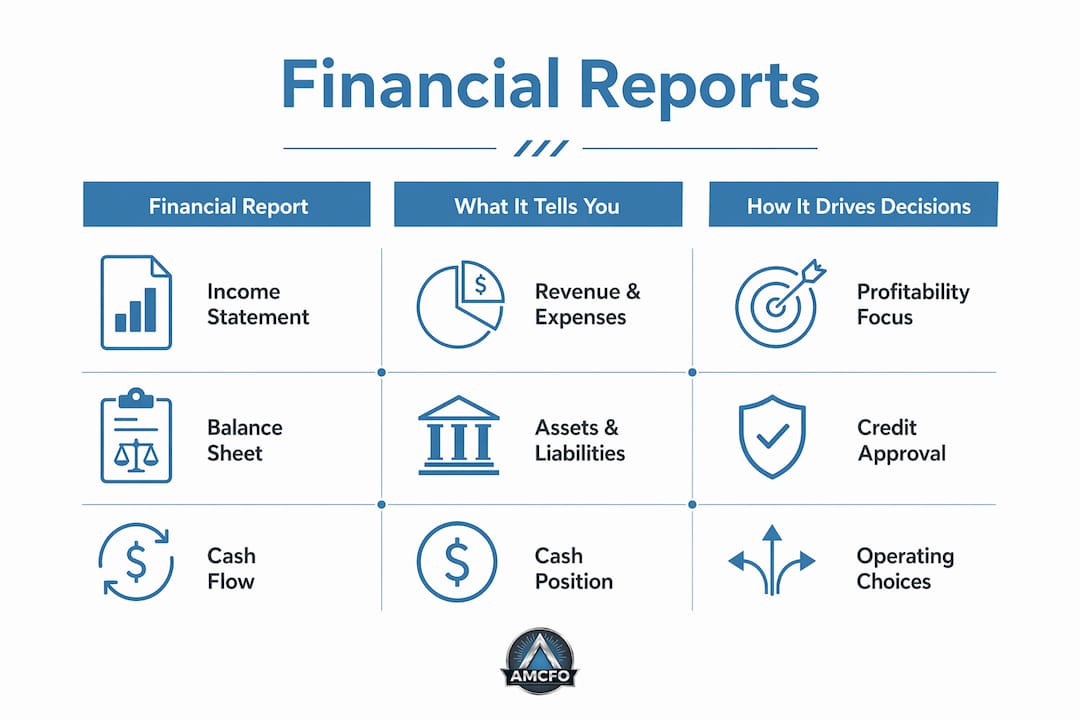

The short answer is yes. Bookkeeping produces the financial reports that every growth decision depends on. The income statement shows whether your business is actually profitable. The balance sheet shows what you own and what you owe. Together, these reports give you the data to budget accurately, forecast realistically, and identify which parts of your business are performing.

Financial reports like balance sheets and income statements are also what banks and creditors review before approving loans or extending credit. Clean, current books signal that your business is well-managed. That signal directly affects your ability to access capital when you need it.

| Financial report | What it tells you | How it drives decisions |

|---|---|---|

| Income statement | Revenue, expenses, and net profit | Identifies which products or services are most profitable |

| Balance sheet | Assets, liabilities, and equity | Shows financial strength for loan applications |

| Cash flow statement | Timing of cash in and out | Prevents shortfalls and guides spending timing |

| Accounts receivable aging | Outstanding customer invoices | Flags collection problems before they hurt cash flow |

Identifying trends is where bookkeeping shifts from record-keeping to real strategy. When you compare month-over-month or year-over-year data, patterns emerge. You see which months are slow, which expense categories are growing faster than revenue, and where your margins are tightest. That information is what separates reactive business owners from proactive ones.

Investor confidence also ties directly to your books. If you ever seek outside funding, investors will ask for financial statements immediately. Businesses with clean, consistent records move through due diligence faster and negotiate from a stronger position.

Pro Tip: Review your income statement and cash flow statement together every month, not just at tax time. Decisions made with current data are almost always better than decisions made from memory.

What bookkeeping methods and tools work best for small businesses?

Double-entry bookkeeping is the standard method used by businesses of every size. Every transaction records a debit in one account and a credit in another. That structure creates a built-in error check because the books must always balance. It is the method required under GAAP and the one that produces the financial statements lenders and investors expect.

Cloud-based bookkeeping software and double-entry bookkeeping improve efficiency and reduce errors significantly compared to manual spreadsheets. Modern platforms connect directly to your bank accounts, import transactions automatically, and flag duplicates before they become problems. That automation cuts the time you spend on data entry and reduces the risk of human error.

The practical benefits of current bookkeeping tools include:

- Automatic bank feeds pull transactions daily so your records are always current

- Receipt capture via mobile apps eliminates paper and matches expenses to categories instantly

- Payroll integration keeps labor costs recorded accurately without manual entry

- Tax-ready reports generate in minutes rather than requiring days of manual preparation

- Multi-user access lets your bookkeeper, accountant, and CFO work from the same live data

For small businesses, the right tool depends on transaction volume and complexity. Entry-level platforms handle basic income and expense tracking well. Businesses with inventory, multiple revenue streams, or payroll typically need a more capable platform with deeper reporting. Amcfo provides QuickBooks setup and cleanup as part of its bookkeeping services, which means you get the right configuration from the start rather than fixing problems later.

Automation in bookkeeping reduces errors and missed opportunities. The time you save on manual data entry is time you can put back into running and growing your business.

Key Takeaways

Accurate, consistent bookkeeping is the single most effective way for small business owners to maintain financial control, reduce tax risk, and make decisions that support real growth.

| Point | Details |

|---|---|

| Financial visibility | Clean books show true cash flow and profitability, not just your bank balance. |

| Tax compliance | Year-round recordkeeping reduces penalties and captures every deductible expense. |

| Growth decisions | Income statements and balance sheets give you the data to budget and forecast accurately. |

| Double-entry method | GAAP-standard double-entry bookkeeping creates built-in error checks and audit-ready records. |

| Monthly reconciliation | Reconciling monthly costs far less than cleaning up disorganized year-end records. |

Bookkeeping is an investment, not a line item to cut

Most small business owners I work with come in treating bookkeeping as something to deal with later. They check their bank balance, assume the business is doing fine, and move on. That habit is exactly how profitable-looking businesses end up with a cash crisis in month nine.

The real cost of neglecting bookkeeping is not the accountant's cleanup bill, though that is real and painful. The real cost is the decisions you make without accurate data. You hire too early, price too low, or miss a tax deduction worth thousands because the expense was never categorized correctly.

What I have seen work consistently is treating bookkeeping the same way you treat your best sales process. You build it, you maintain it, and you use the output to make better decisions every month. Successful businesses treat bookkeeping as a strategic investment that frees owner time for core operations and growth. That is not accounting theory. That is what separates businesses that scale from ones that stay stuck.

If you are a small business owner reading this and your books are more than 30 days behind, that is the first thing to fix. Not your marketing, not your hiring plan. Your books. Everything else gets clearer once you can see the actual numbers. For a practical starting point, the bookkeeping guide for entrepreneurs covers exactly how to build that foundation from the ground up.

— Angelica

Accurate books are the foundation Amcfo builds on

Running a business without current financial records creates risk at every level, from tax penalties to missed growth opportunities.

Amcfo provides bookkeeping, accounting, and fractional CFO services built specifically for small businesses that need financial clarity without hiring a full-time finance team. Services include monthly bookkeeping, QuickBooks setup and cleanup, payroll support, tax coordination, and financial reporting that gives you real numbers to work with. Whether your books need a fresh start or ongoing maintenance, Amcfo's accounting and bookkeeping services are designed to keep your business organized, compliant, and positioned to grow. Reach out to Amcfo to get your finances working for you.

FAQ

What is bookkeeping and why does it matter?

Bookkeeping is the process of recording and organizing all financial transactions a business makes. It matters because accurate records support tax compliance, cash flow management, and every major financial decision.

How does bookkeeping help with taxes?

Organized bookkeeping ensures every deductible expense is captured and correctly categorized, which reduces your tax bill and lowers the risk of IRS penalties or audit exposure.

What is double-entry bookkeeping?

Double-entry bookkeeping records every transaction as both a debit and a credit, creating a built-in error check. It is the standard method required under GAAP and used to produce financial statements.

How often should a small business reconcile its books?

Monthly reconciliation is the best practice. It catches errors early, keeps records audit-ready, and costs far less than cleaning up a full year of disorganized records at tax time.

Can bookkeeping help a small business grow?

Yes. Financial reports produced through consistent bookkeeping reveal profitability trends, support accurate budgeting, and give lenders and investors the data they need to extend credit or funding.